Do falling oil prices raise the threat of deflation?

The spectacular drop in oil prices means that inflation is going to fall even further below the Fed’s 2% target. Does that raise any new risks for the economy? I say no, and here’s why.

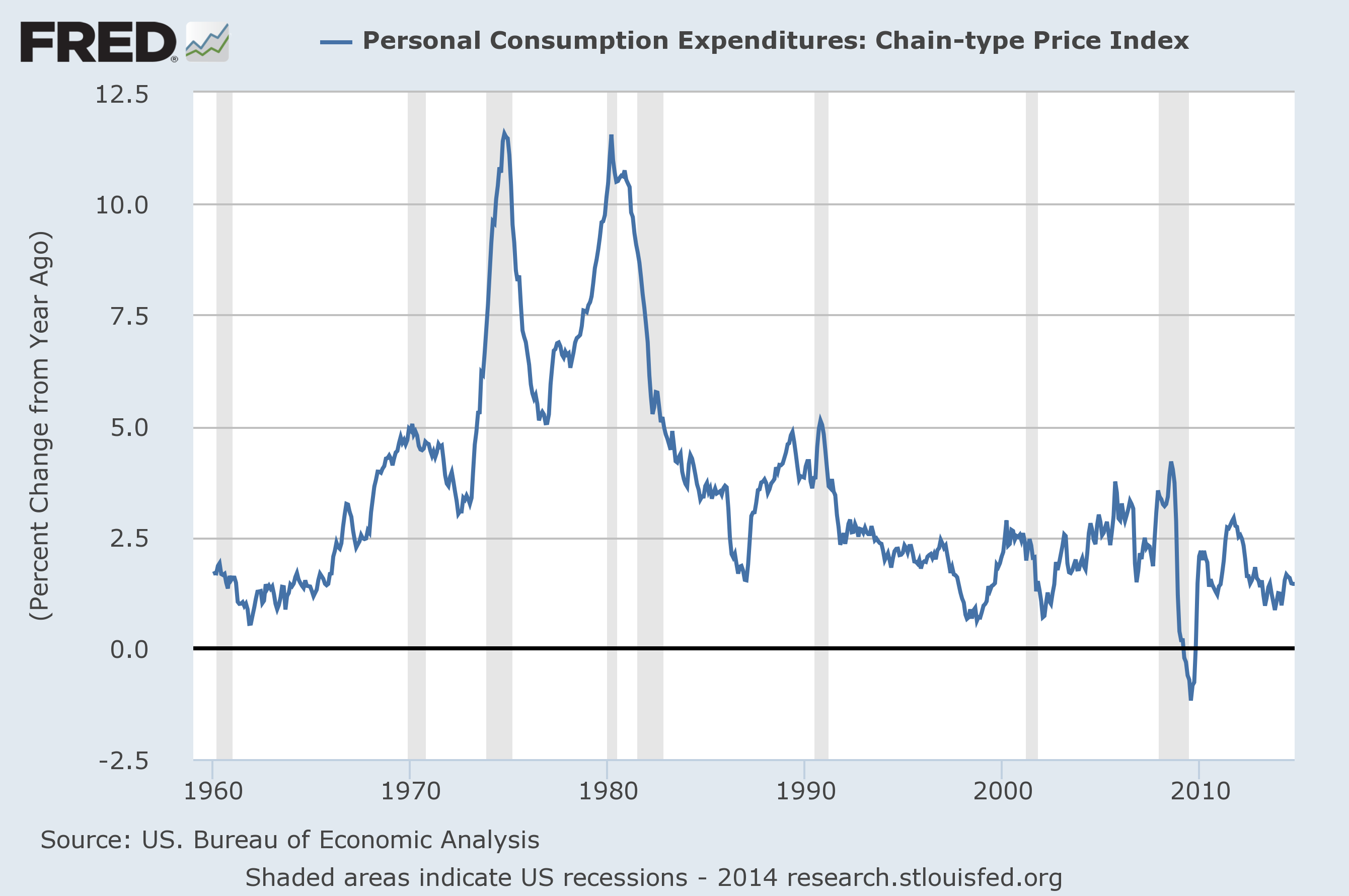

Year-over-year percent change in the monthly deflator for personal consumption expenditures. Source: FRED.

In economists’ theoretical models, inflation usually is often thought of as a condition in which all wages and prices move up together by the same amount. For a given nominal interest rate, the lower inflation, the higher is the real cost of borrowing. With the short-term nominal interest rate still stuck at zero, a decrease in inflation could discourage spending, something the Fed would rather not see happen in the current situation. Or so the theory goes.

But typical consumers often have something very different in mind when they talk about inflation. Many people think of inflation as a condition where the cost of the goods and services they buy goes up but their wages do not. Not so surprising then that while the Fed says it wants more inflation, most consumers say they do not.

What’s happened to oil prices this fall looks more like the average Joe’s version of reality than the Fed’s. The average U.S. retail price of gasoline right now is about $2.40 a gallon. Last year American consumers and businesses bought 135 billion gallons of gasoline at an average price of $3.60 a gallon. If gasoline prices stay where they are and if we buy the same number of gallons of gasoline this year as last, that leaves us with an additional $160 billion to spend over the course of the year on other items. If we restate the total savings for U.S. consumers and businesses in terms of the 116 million U.S. households, that works out to almost $1,400 per household.

To read more, go to the Seeking Alpha website.

This article is published in collaboration with Seeking Alpha. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with Forum:Agenda subscribe to our weekly newsletter.

Author: James D. Hamilton has been a professor in the Economics Department at the University of California at San Diego since 1992.

Image: A worker fills the tank of a car at a petrol station in Cairo, March 12, 2013. REUTERS/Mohamed Abd El Ghany.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Oil and Gas

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Council on the Future of Growth and 2023-2024

December 20, 2024