Why are labour market recoveries getting weaker?

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

United States

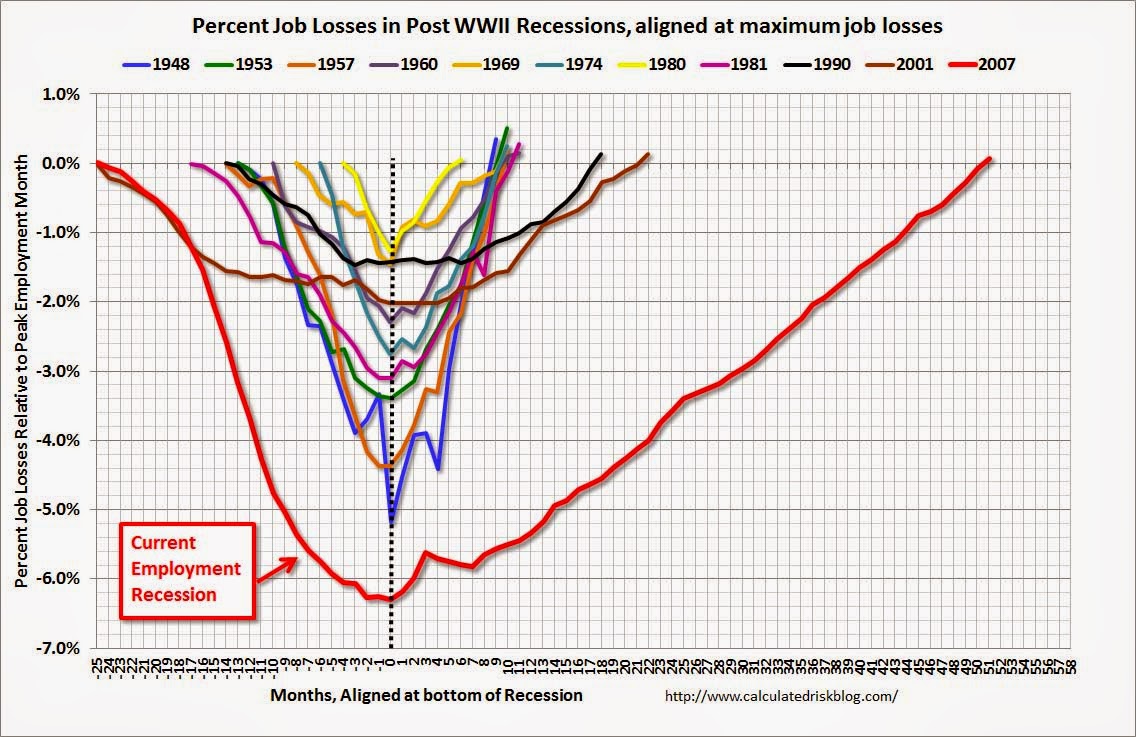

The slow U.S. labor market recovery from the Great Recession is a well-known, oft-lamented, and thought-provoking phenomenon. A famous graph by writer Bill McBride shows how long it has taken the labor market to return to its previous employment peak level: 51 months, or just over 4 years. The graph actually overstates the recovery, which is considerably slower than any other since the end of WWII, because it doesn’t account for population growth.

But notice that the two weakest recoveries before this one were those following the two most recent recessions, starting in 2001 and 1990. Labor market recoveries are becoming weaker and weaker. Paul Krugman has called these recoveries “postmodern.” But what is causing this decline in employment growth? A new paper argues that the decline in new businesses, or startups, could be responsible.

The paper is authored by economists Benjamin Pugsley and Ayşegül Şahin, both of the Federal Reserve Bank of New York. The authors document the increasing age of businesses in the United States. What has happened since the mid-1980s is not that new business are more likely to fail or that they growth more quickly. Rather, the rate at which startups enter has fallen. What the labor market is left with is employment residing in more “grown-up” firms.

Shifting employment toward older firms could boost growth. Because “grown-up firms” are less affected by recessions, older firms have higher growth rates and smoother changes in employment. Or the effects could go the other way. A lack of startups could hinder employment growth, make employment growth more sensitive to economic recessions and mute the strength of employment recoveries.

The impact of this trend on labor markets isn’t clear until one looks at the data. When Pugsley and Şahin look closely, they find the negative effects from this startup deficit outweigh the benefits of having more employment in older firms. In particular, the impact of the startup deficit on business cycles fits in line with jobless recoveries: employment growth falls much more during recessions and employment doesn’t pick up as much when gross domestic product starts growing again. The authors calculate that if the startup rate were equal to its average from 1980 to 1985 then the employment recovery would be two years ahead of where it is now.

If Pugsley and Şahin’s research is correct, the labor market is suffering significantly from a lack of startups. But this isn’t to say this deficit is the only reason for jobless recoveries. The build-up in private debt and collapse of asset bubbles that Krugman highlights could be responsible as well. The fall-off in consumption independently reduces employment demand, and may in fact also be a cause of the decline in the startup rate. Or it could be another reason altogether. But at the moment, no one is quite sure by how much each factor is affecting the slowdown. Sifting through these different hypotheses is a critical task for future research.

This article is published in collaboration with The Washington Center for Equitable Growth. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with Forum:Agenda subscribe to our weekly newsletter.

Author: Nick Bunker is a Policy Research Associate with the Washington Center for Equitable Growth.

Image: An instructor (L) teaches trainees at a maritime transport training centre, which offers classes as part of a government-sponsored programme to train unemployed people in industrial professions, in Alexandria April 30, 2014. REUTERS/Stringer.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Geo-Economics and PoliticsSee all

Robin Pomeroy

July 18, 2024

Spencer Feingold and Simon Torkington

July 5, 2024

Pooja Chhabria

June 27, 2024

Spencer Feingold

June 27, 2024

Spencer Feingold

June 26, 2024

{kind=link}