How does VAT affect the behaviour of small companies?

Stay up to date:

Future of Work

Most countries around the world use a value added tax (VAT) as their primary indirect tax, and most countries have thresholds based on turnover – the value of goods and services a business provides – below which businesses do not need to register for VAT. In the EU, all but two countries (Spain and Sweden) have registration thresholds. The UK’s threshold of £81,000 is the EU’s highest, and is perceived as a way for the government to reduce the compliance costs of small businesses not wishing to register for VAT. However, thresholds are generally much higher in countries that have introduced VAT more recently, such as Singapore, which currently has a threshold of about €540,000.

In the wake of the Global Crisis, many governments turned to VAT to fill the hole in their public finances, either by increasing the standard VAT rate or by lowering the registration threshold. In the UK, for instance, VAT generates 21% of total tax revenue, ranking it behind only income tax and national insurance contributions as the largest source of tax revenue. Generally, registration involves an increase in tax liability for the firm and also compliance costs, which may not be trivial. In the UK, compliance costs for a firm with turnover at the VAT threshold are estimated to be around 1-2% of turnover, and the cost may be higher in other countries.

Effects of VAT on the behaviour of small firms

Thus, a key question to inform policymaking is how VAT itself and, in particular, the registration threshold affect the behaviour of small firms. We aim to understand the efficiency and welfare costs of VAT by analysing three important, behavioural responses to the registration threshold: voluntary registration, bunching, and growth effects.

Voluntary registration makes VAT unique amongst all the major taxes. It refers to a situation where a firm registers for VAT even if it is below the turnover threshold, and thus is not required to do so. This is likely to occur when a firm has large purchases of intermediate inputs, and/or they can pass most of the VAT on output onto the purchaser. In this case, it may be profitable to voluntarily register for VAT so the firm can claim back input tax, while passing some or most of the burden of the output tax on to the purchaser. In our comprehensive UK dataset, further described below, over 44% of companies in the UK with turnover below the threshold register voluntarily.

However, not all firms are in this position. A small trader selling services to households, such as a plumber or electrician, might have relatively small purchases of intermediate inputs and face elastic demand from purchasers, who themselves cannot claim back the VAT that they pay. In this case bunching occurs, where a firm keeps its reported taxable turnover just below the registration threshold either legally, by restricting the scale of its operations, or illegally, by misreporting sales. Growth effects are related to bunching and occur when the firm restricts its growth in order to keep below the threshold and possibly also has a higher rate of ‘catch-up’ growth when it decides to register.

Several papers in the academic and policy literature have argued conceptually that voluntary registration, bunching, and growth effects might exist. For example, the ground-breaking VAT model by Keen and Mintz (2004) found bunching below the threshold and a hole above where firms do not locate. However, voluntary registration is never optimal in their model because none of the burden of output VAT can be passed on to purchasers. Brashares et al. (2014) discuss some of the possible determinants of voluntary registration and bunching in their calibration of the Keen-Mintz model to US data, but they are unable to test the predictions with data because the US has no VAT. To date, no work has yet established the extent to which these effects actually occur, their magnitudes, and their determinants for a country where VAT is in place.

Behavioural responses to VAT: New framework

To fill in these gaps, we develop a conceptual framework for studying the two key aspects of behavioural response to VAT, including voluntary registration and bunching, and we test this framework using UK firm-level data on tax returns and firm characteristics.

- We show that voluntary registration is more likely in two scenarios: when the cost of inputs relative to sales is high, or when the proportion of business-to-consumer (B2C) sales is low.

In the first scenario, when input costs are important, registration allows the firm to claim back a considerable amount of input VAT. In the second, if most customers are VAT-registered, the burden of an increase in VAT can easily be passed on in the form of a higher price, because the customer himself can claim back the increase.

We show that the determinants of bunching at the registration threshold are the same as for voluntary registration, with the signs of the effects reversed.

- Specifically, bunching is more likely when the cost of inputs relative to sales is low, or when the proportion of business-to-consumer sales is high.

We also show that the elasticity of value added of registered firms with respect to the effective VAT rate can be recovered from an implicit function that relates the degree of bunching to the elasticity of value added.

Finally, we show in the conceptual framework that the elasticity of value added can be related in a simple way to the deadweight loss of a small increase in the statutory rate of VAT, thus extending the well-known results of Feldstein (1999) and Chetty (2009) to an indirect tax setting.

We bring these predictions to an administrative dataset created by linking the population of corporation and VAT tax records in the UK, which includes 1,408,517 observations for 435,688 companies between 1 April 2004 and 30 March 2010. We show that the empirical pattern of voluntary registration is consistent with the theory. In particular, voluntary registration is more likely with a low share of business-to-consumer sales or a high share of input costs.

Quantitatively, the probability that a firm voluntarily registers for VAT is increased by 0.05 for a one standard deviation increase in the share of business-to-consumer sales, and by 0.02-0.05 for a one standard deviation increase in the input-cost ratio.

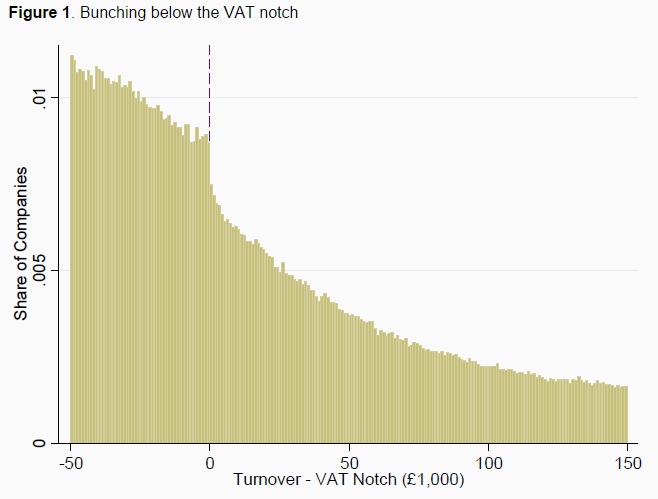

We then look at bunching. To get a feel for the data, Figure 1 below shows a histogram of the distribution of firm turnover, pooling data across all years. To allow comparison across years, we measure turnover in deviations from the threshold in any given year. As Figure 1 shows, there is clear evidence of bunching at the VAT threshold, shown by the dotted line, which is mainly driven by growing firms. This is the first evidence, to our knowledge, that a VAT notch leads to bunching.

Figure 1. Bunching below the VAT notch

Investigating further we find that, consistent with the theory, firms are more likely to bunch at the threshold when either the cost of inputs relative to sales is high, or when the proportion of business-to-consumer sales is low. So there is a clear pattern of heterogeneity in bunching.

What are the mechanisms behind the bunching?

The next question concerns how firms bunch, that is, what are the mechanisms at work? One possibility is that they genuinely restrict their sales to stay below the threshold. If so, the distribution of the input-cost ratio should be smooth around the VAT notch. We provide some suggestive evidence that part of the bunching is driven by under-reporting of sales. Specifically, we find that the salary-inclusive input-cost ratio moves in parallel between the registered and non-registered group outside the bunching region, but starts to increase substantially for the non-registered companies just below the threshold. We interpret the large and sharp increase in the salary-inclusive input-cost ratio to be partly driven by the fact that it is costly to under-report salary expenses due to third-party reporting.

In ongoing work, we are addressing the effects of the registration threshold on small firm growth. There is a vast empirical literature on the determinants of small-to-medium enterprise (SME) growth, but relatively little attention has been given to the role of ‘tax notches’ such as VAT registration. If we consider the analogue of Figure 1 just for firms that are growing, we see that bunching is much sharper, suggesting that the threshold might inhibit firm growth.

Figure 2. Bunching by growing firms

We find that firms with a turnover below the VAT threshold that are not registered for VAT have a significantly lower growth rate than a ‘control group’ of firms below the threshold that are voluntarily registered for VAT (and thus do not have a tax cost of registration). Firms that cross the VAT threshold in a given year have a higher growth rate in that year than a control group of firms already above the threshold. Moreover, the closer the ‘treated’ firms are to the threshold, the stronger these effects are.

References

Brashares E, M J Knittel, G Silverstein and A Yuskavage (2014), “Calculating the Optimal Small Business Exemption Threshold for a US VAT”, National Tax Journal 67(2), pp. 283-320.

Feldstein, M (1999), “Tax Avoidance and the Deadweight Loss of the Income Tax”, The Review of Economics and Statistics 81(4): 674.680.

Kumar K B, R G Rajan and L Zingales (1999), “What determines firm size?” NBER Working Paper No. 7208.

Liu, L and B Lockwood (2015), “VAT Notches”, CEPR Discussion Paper 10606.

Keen, M and J Mintz (2004), “The Optimal Threshold for a Value-Added Tax”, Journal of Public Economics 88(3-4), pp. 559-576.

Saez, E (2010), “Do Taxpayers Bunch at Kink Points?”, American Economic Journal: Economic Policy 2(3), pp. 180-212.

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Authors: Li Liu is a Senior Research Fellow at the Oxford University Centre for Business Taxation. Ben Lockwood is Professor of Economics at Warwick University.

Image: U.S. one dollar bills blow near the Andalusian capital of Seville in this photo illustration taken on November 16, 2014. REUTERS/Marcelo Del Pozo.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Erik Crouch

July 1, 2025

Stephanie Holmes, Pooja Chhabria and John Letzing

June 26, 2025

Chris Hamill-Stewart

June 25, 2025

Tariq Bin Hendi

June 25, 2025

John Letzing

June 25, 2025