How the business cycle affects your career

Workers often build their careers through job-hopping. Over time, they tend to move toward higher paying jobs that last longer (Topel and Ward 1992). These career paths are facilitated by job-to-job flows:1 when a worker has a better offer from a different employer, she will usually quit her job to take the new, better one.

A number of studies have established that the pace of both quits and job-to-job transitions are highly procyclical (Farber 1999, Fallick and Fleischman 2004, Hall 2005). When unemployment is low, more workers quit their jobs, and there are more job-to-job flows. During the labour market contractions associated with the 2001 and 2007-2009 recessions, quits and job-to-job flows declined sharply. In the aftermath of the most recent recession, job-to-job flows fell to historic lows and have been slow to recover (Hyatt and Spletzer 2013, Davis and Haltiwanger 2014, Figure 2 of Haltiwanger et al. 2015a). A simple forecast of the most recent years of data (i.e. assuming the most recently observed trend continues) indicates that job-to-job flows will not recover to levels seen in the year 2000 until 2018.

Recent research has sought to better understand how these job-to-job flows translate into enhanced productivity and earnings gains, and how these patterns vary over the cycle. Economic theories of on-the-job search suggest workers will move up the job ladder from lower-paying, less productive firms towards higher-paying, more productive firms. A corollary implication is that such flows will also be from small to large firms, since theory implies that firms that are more productive will be larger and higher paying. The implied close relationship between firm size, productivity and wages has received some empirical support.2 Theory also suggests these job-to-job flows should intensify during booms implying that one of the costs of recessions is the slowdown of workers moving up the job ladder ( Moscarini and Postel-Vinay 2009, 2012).

In a recent study (Haltiwanger et al. 2015a), we use new measures of job-to-job flows from rich matched employer-employee administrative data to quantify the nature and extent of these flows by firm size and firm wages over the cycle. This new data source allows us to decompose hires and separations into those stemming from job-to-job flows and those related to non-employment. We do this by firm wage and by firm size (see Figures 4 and 5 of Haltiwanger et al. 2015a).

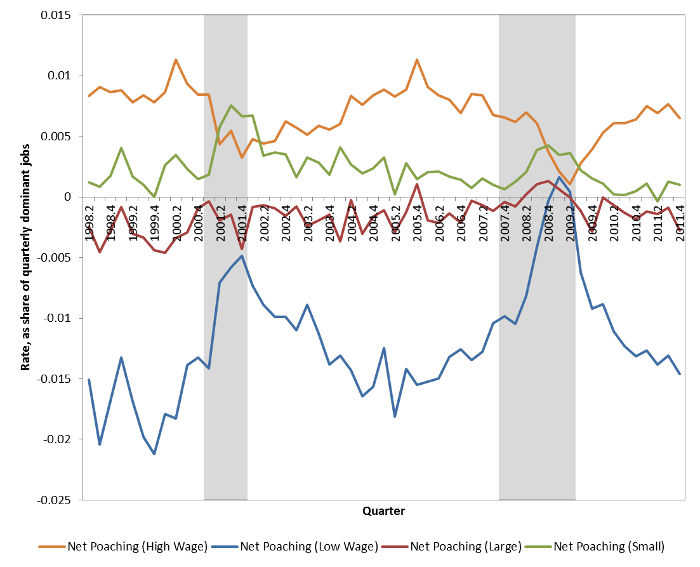

Consistent with economic theory, we find strong evidence for a cyclical job ladder by firm wage. If a firm is at the top of a job ladder, and it is able to poach workers from other firms, then the hires that are associated with job-to-job flows should exceed the separations associated with such flows. This is exactly what we find for high-wage firms. Furthermore, the high-wage firms are net losers to non-employment. In addition, the positive net poaching by high-wage firms has a pronounced procyclical pattern. During booms, high-wage firms gain the most from net poaching. During recessions and especially during the Great Recession, the gains from net poaching by high-wage firms collapses.

The opposite patterns hold for low-wage firms. For these firms, poaching separations consistently exceed poaching hires, and this net loss through poaching is lower during contractions. Low-wage firms gain workers on net through hires from non-employment. These findings highlight that an important cost of recessions is the sharp slowdown in workers moving up the job ladder.

In contrast, the evidence is not consistent with a cyclical job ladder by firm size. Large firms consistently have more separations associated with job-to-job flows than hires, indicating that they are net losers through poaching. Small firms, by contrast, are positive net poachers. Both large and small firms usually have more hires from non-employment than separations to non-employment.

The net poaching gains and losses through job-to-job flows are illustrated in Figure 1 by firm size and firm wage (from Figure 6 of Haltiwanger et al. 2015a). High-wage firms have net poaching gains that are larger during expansions, while low-wage firms have net poaching losses that shrink during contractions. Furthermore, because of the strong convergence between the net poaching of high-wage and low-wage firms during contractions, we can see how the firm wage job ladder shuts down in the Great Recession. There is not nearly as much cyclicality in either of the net poaching lines for these two firm size categories, and net poaching for small firms is consistently higher than for large firms.

Figure 1. Net poaching by firm size and firm wage

Source: Figure 6 of Haltiwanger et al. 2015a.

Why are there such different findings by firm size and firm wage? Part of this is because young firms usually start small, and some of those small, young firms turn out to be highly productive and grow rapidly and poach workers away from other firms. It turns out that small, mature firms (those aged ten years or more) lose workers, on net, through poaching while young firms gain workers, on net, from poaching. Additionally, there is an important segment of large firms that offer low wages (e.g. in the retail trade sector). Those large, low-wage firms tend to hire non-employed workers, and this hiring shuts down during recessions. Moreover, workers at large, low-wage firms are often poached away by other firms. Understanding the factors that drive a wedge in the relationship between firm size, firm productivity and firm wages should be an active area for future research. Our findings suggest researchers should be cautious about using firm size as a proxy for productivity and wages in studying the dynamics of the economy.

Cyclical job ladders

In recent years, we have learned a lot about how to characterise and assess cyclical job ladders in the labour market. There is clearly a pro-cyclical job ladder among firms by the wages offered. Other evidence in recent papers has found job ladders by firm productivity (Haltiwanger et al. 2015b) as well as across occupations by wages paid and industries by value added (Cairo et al. 2015). The evidence shows that, during labour market downturns, workers tend to stay for longer on lower-paying, less productive rungs of the job ladder.

References

Brown, C, and J Medoff (1989), “The Employer Size-Wage Effect”, Journal of Political Economy97(5): 1027-1059.

Cairo, I, H Hyatt, and N Zhao (2015), “The U.S. Job Ladder in the New Millennium”, 2015 Society for Economic Dynamics Conference in Warsaw, Poland.

Davis, S, and J Haltiwanger (2014), “Labor Market Fluidity and Economic Performance”, NBER Working Paper #20479, Proceedings of the Jackson Hole Symposium, Federal Reserve Bank of Kansas, available athttps://www.kansascityfed.org/publicat/sympos/2014/2014Davis_Haltiwanger….

Fallick, B, Fleischman, C A (2004), “Employer-to-Employer Flows in the U.S. Labor Market: The Complete Picture of Gross Worker Flows”, FEDS Working Papers 2004-34, Federal Reserve Board.

Farber, H (1999), “Mobility and Stability: The Dynamics of Job Change in Labor Markets”, in O Ashenfelter and D Card (eds.) Handbook of Labor Economics vol. 3B, Amsterdam: Elsevier, 2439-2484.

Hall, Robert (2005), “Employment Efficiency and Sticky Wages: Evidence from Flows in the Labor Market”, Review of Economics and Statistics 87(3): 397-407.

Haltiwanger, J C, H R Hyatt, and E McEntarfer (2015a), “Cyclical Reallocation of Workers Across Employers by Firm Size and Firm Wage”, NBER Working Paper #21235.

Haltiwanger, J, H Hyatt, and E McEntarfer (2015b), “Firm Size, Wages, and Productivity”, 2015 Society of Labor Economists Conference in Montreal, Canada.

Hyatt, H R, and J R Spletzer (2013), “The Recent Decline in Employment Dynamics”, IZA Journal of Labor Economics 2(5): 1-21.

Moscarini, G, and F Postel-Vinay (2009), “The Timing of Labor Market Expansions: New Facts and a New Hypothesis”, in D Acemoglu, K Rogoff, and M Woodford (eds.) NBER Macroeconomics Annual, Vol. 23, 1-52, Chicago: University of Chicago Press.

Moscarini, G, and F Postel-Vinay (2012), “The Contribution of Large and Small Employers to Job Creation in Times of High and Low Unemployment”, American Economic Review 102(6): 2509-39.

Syverson, C (2011), “What Determines Productivity?”, Journal of Economic Literature 49(2): 326-365.

Topel, R H, and M P Ward (1992), “Job Mobility and the Careers of Young Men”, Quarterly Journal of Economics 107(2): 439-479.

Footnotes

1 Job-to-job flows are sometimes called ‘employer-to-employer flows’

2 For evidence that larger firms pay higher wages, see Brown and Medoff (1989). For a summary of evidence that more productive firms are larger, see Syverson (2011).

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: John C. Haltiwanger, is a Professor in the Department of Economics at the University of Maryland. Henry R. Hyatt is a Senior Economist in the Center for Economic Studies at the U.S. Census Bureau. Erika McEntarfer is the Lead Economist for the Longitudinal Employer-Household Dynamics Research Group at the U.S. Census Bureau’s Center for Economic Studies.

Image: A man using his mobile phone stands near a glass window at a building at a Tokyo’s business district March 18, 2015. REUTERS/Yuya Shino

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Future of Work

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Jobs and the Future of WorkSee all

Amitabh Chaudhry

January 10, 2025