5 things to know about Canada’s economy

Stay up to date:

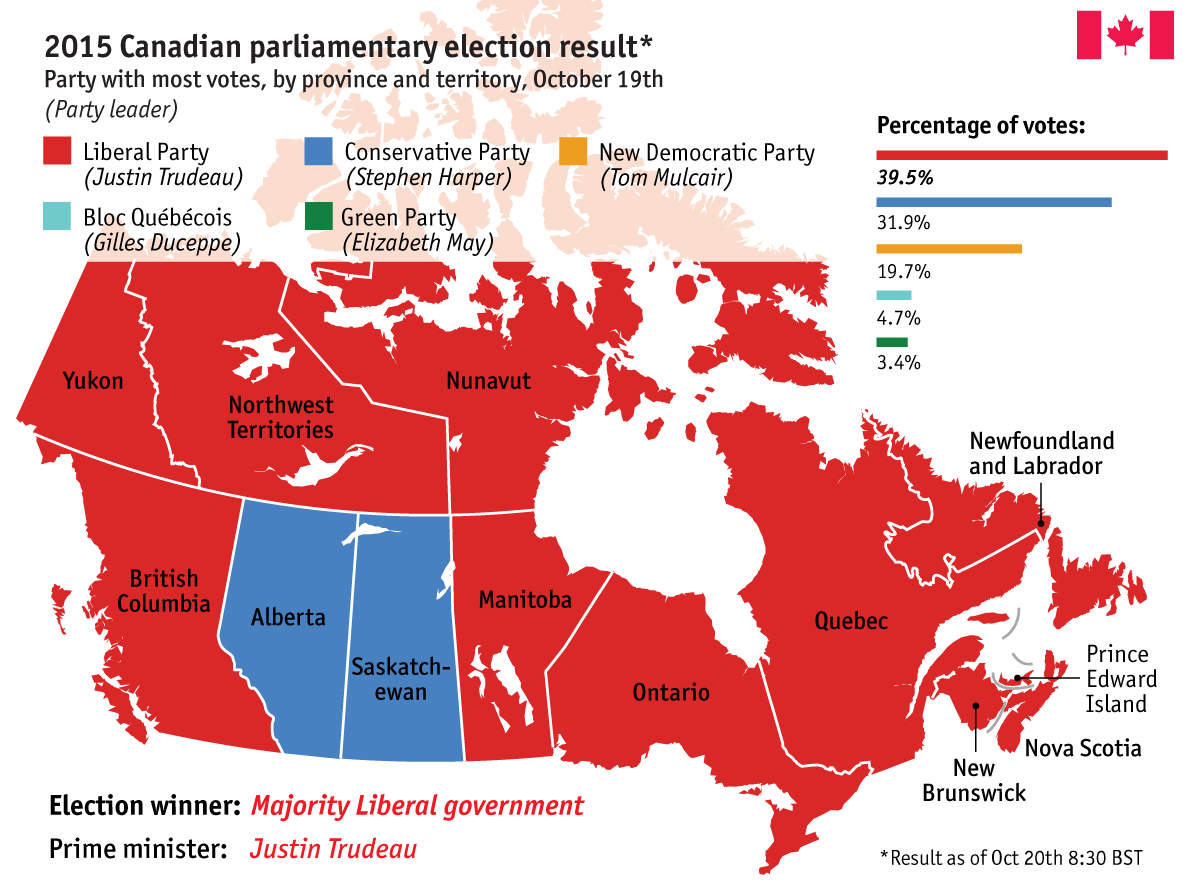

Canada

The sweeping election victory of Justin Trudeau’s Liberal Party has thrust Canada’s economic woes into the global spotlight.

Source: Election Canada; The Economist

The commodity-based economy is technically in a recession, owing in part to this year’s fall in oil prices. But the country is also suffering from deeper structural problems. Addressing these challenges and building an economy for the 21st century are among the key challenges facing Canada’s new prime minister.

Reliance on crude oil

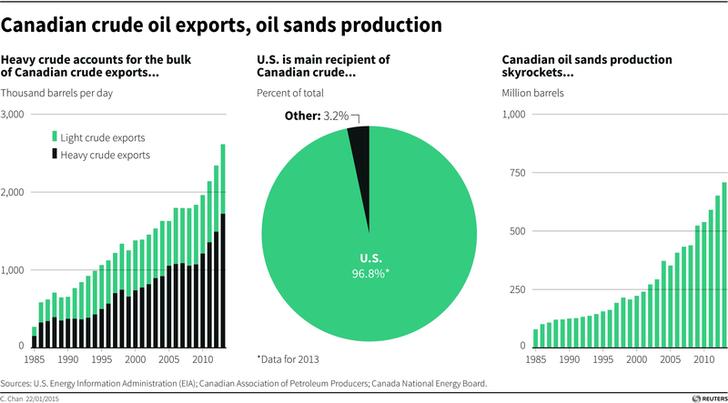

Canada’s economy, ranked 11th in the world by GDP, has focused on resource extraction in recent years. While crude oil, Canada’s big commodity export, helped the country get through the global financial crisis relatively unscathed, the low oil price is now putting the economy under severe strain. This year, Canada’s economic performance has been the worst among a small group of developed economies that depend heavily on resources, such as Norway and Australia. Between June 2014 and July 2015, revenue from Canadian energy exports decreased 34.6%, forcing producers to cut back on jobs and investments.

Structural problems

The drop in global energy prices is not the only reason for Canada’s sluggish economy. There is much hand-wringing over Canada’s lack of innovative, globally competitive companies at a time when its traditional manufacturing industries are being eroded. Canada trails other developed economies in areas including corporate research and development, information technology investments, patents and productivity.

Debt and overvalued housing

There are concerns that ultra-low interest rates, currently at 0.5%, have been driving unsustainable housing booms, particularly in Toronto and Vancouver.

Consumer debt is at a record 165% of disposable income, with most of the borrowing going into buying houses. Bank of Canada Governor Stephen Poloz said that increasing levels of household debt represent “a key vulnerability for the financial system”.

Budget deficits and spending

Canada’s recession made stimulating economic growth a key topic in the election. Conservative leader Stephen Harper, who stepped down after almost a decade in power, pledged to run a balanced budget. In contrast, Trudeau said he would tackle the economic downturn by running budget deficits of $25 billion over the next three years to fund infrastructure. The incoming prime minister has also pledged to cut income taxes for middle-class Canadians while increasing them for the wealthy.

The Keystone oil pipeline

Mr Trudeau plans to address environmental concerns over proposals for the controversial Keystone oil pipeline, which has put relations between the US and Canada under strain. Mr Harper had hoped the pipeline, which would carry crude from Alberta to Texas, would create jobs, but President Obama vetoed the plan.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Rosamond Hutt is a Senior Producer at Formative Content.

Image: A view of downtown Montreal from the Kondiaronk Belvedere mountain top lookout and the Chalet du Mont Royal, August 12, 2009. REUTERS/Benoit Tessier

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Rya G. Kuewor

May 13, 2025

Tea Trumbic and Dhivya O’Connor

May 13, 2025

Navi Radjou

May 8, 2025

Dave Neiswander

April 28, 2025

Alem Tedeneke

April 25, 2025

Michael Eisenberg and Francesco Starace

April 25, 2025