Is Europe’s financial crisis pushing voters to the far-right?

This article is published in collaboration with Project Syndicate.

I may not be the only finance professor who, when setting essay topics for his or her students, has resorted to a question along the following lines: “In your view, was the global financial crisis caused primarily by too much government intervention in financial markets, or by too little?” When confronted with this either/or question, my most recent class split three ways.

Roughly a third, mesmerized by the meretricious appeal of the Efficient Market Hypothesis, argued that governments were the original sinners. Their ill-conceived interventions – notably the US-backed mortgage underwriters Fannie Mae and Freddie Mac, as well as the Community Reinvestment Act – distorted market incentives. Some even embraced the argument of the US libertarian Ron Paul, blaming the very existence of the Federal Reserve as a lender of last resort.

Another third, at the opposite end of the political spectrum, saw former Fed Chairman Alan Greenspan as the villain. It was Greenspan’s notorious reluctance to intervene in financial markets, even when leverage was growing dramatically and asset prices seemed to have lost touch with reality, that created the problem. More broadly, Western governments, with their light-touch approach to regulation, allowed markets to career out of control in the early years of this century.

The remaining third tried to have it both ways, arguing that governments intervened too much in some areas, and too little in others. Avoiding the question as put is not a sound test-taking strategy; but the students may have been onto something.

Now that the crisis is seven years behind us, how have governments and voters in Europe and North America answered this important question? Have they shown, by their actions, that they think financial markets need tighter controls or that, on the contrary, the state should repudiate bailouts and leave financial firms to face the full consequences of their own mistakes?

From their rhetoric and regulatory policies, it would appear that most governments have ended up in the third, fence-sitting camp. Yes, they have implemented a plethora of detailed controls, scrutinizing banks’ books with unprecedented intensity and insisting on approving cash distributions, the appointment of key directors, and even job descriptions for board members.

But they have ruled out any future government or central-bank support for ailing financial institutions. Banks must now produce “living wills” showing how they can be wound down without the authorities’ support. The government will wash its hands of them if they run into trouble: the era of “too big to fail” is over.

Perhaps this two-track approach was inevitable, though it would be good to know the desired end-point. Is it a system in which market discipline again dominates, or will regulators sit on the shoulders of management for the foreseeable future?

But what have voters concluded? In the first wave of post-crisis elections, the message was clear in one sense, and clouded in another. Whichever government was in power when the crisis hit, whether left or right, was booted out and replaced by a government of the opposite political persuasion.

That was not universally true – see Germany’s Angela Merkel – but it certainly was true in the United States, the United Kingdom, France, and elsewhere. France moved from right to left, and the UK went from left to right. But voters’ verdict on their governments was more or less identical: things went wrong on your watch, so out you go.

But now we can see a more consistent trend developing. Three German economists, Manuel Funke, Moritz Schularik, and Christoph Trebesch, have just produced a fascinating assessment based on more than 800 elections in Western countries over the last 150 years, the results of which they mapped against 100 financial crises. Their headline conclusion is stark: “politics takes a hard right turn following financial crises. On average, far-right votes increase by about a third in the five years following systemic banking distress.”

The Great Depression of the 1930s, which followed the Wall Street crash of 1929, is the most obvious and worrying example that comes to mind, but the trend can be observed even in the Scandinavian countries, following banking crises there in the early 1990s. So seeking to explain, say, the rise of the National Front in France in terms of President François Hollande’s personal and political unpopularity is not sensible. There are greater forces at work than his exotic private life and inability to connect with voters.

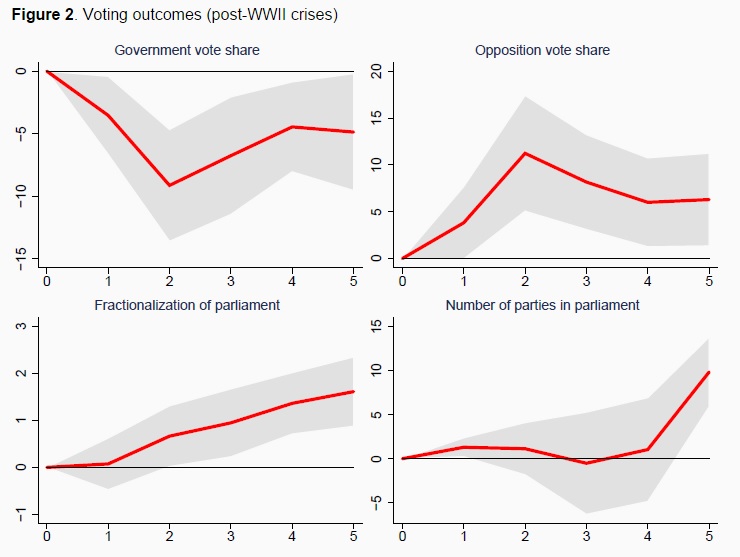

The second major conclusion that Funke, Schularik, and Trebesch draw is that governing becomes harder after financial crises, for two reasons. The rise of the far right lies alongside a political landscape that is typically fragmented, with more parties, and a lower share of the vote going to the governing party, whether of the left or the right. So decisive legislative action becomes more challenging.

At the same time, a surge of extra-parliamentary mobilization occurs: more and longer strikes and more and larger demonstrations. Control of the streets by government is not as secure. The average number of anti-government demonstrations triples, the frequency of violent riots doubles, and general strikes increase by at least a third. Greece has boosted those numbers recently.

The only comforting conclusion that the three economists reach is that these effects gradually peter out. The data tell us that after five years, the worst is over. That does not seem to be the way things are moving now in Europe, if we look at France’s recent election scare, not to mention Finland and Poland, where right-wing populists have now come to power. Maybe the answer is that the clock starts ticking on the five years when the crisis is fully over, which is not yet true in Europe.

So politics seems set to remain a difficult trade for some time. And the bankers and financiers who are widely blamed for the crisis will remain in the sin bin for a while yet, until voters’ expectations of economic and financial stability are more consistently satisfied.

Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Howard Davies, the first chairman of the United Kingdom’s Financial Services Authority (1997-2003), is Chairman of the Royal Bank of Scotland.

Image: European Union flags fly outside the European Commission headquarters in Brussels. REUTERS/Thierry Roge.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Global Governance

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Geographies in DepthSee all

Naoko Tochibayashi and Mizuho Ota

December 23, 2024