The Euro turns 20. What have we learned from it?

Happy birthday, Euro! Image: REUTERS/Leonhard Foeger

The euro’s first 20 years played out very differently than many expected, highlighting the importance of recognizing that the future is likely to be different from the past. Given this, only a commitment to flexibility and a willingness to rise to new challenges will ensure the common currency’s continued success.

Twenty years ago this month, the euro was born. For ordinary citizens, little changed until cash euros were introduced in 2002. But in January 1999, the “third stage” of Economic and Monetary Union officially started, with the exchange rates among the original 11 eurozone member states “irrevocably” fixed, and authority over their monetary policy transferred to the new European Central Bank. What has unfolded since then holds important lessons for the future.

In 1999, conventional wisdom held that Germany would incur the biggest losses from the euro’s introduction. Beyond the risk that the ECB would not be as tough on inflation as the Bundesbank had been, the Deutsche Mark was overvalued, with Germany running a current-account deficit. Fixing the exchange rate at that level, it was believed, would pose a severe challenge to the competitiveness of German industry.

Yet, 20 years on, inflation is even lower than it was when the Bundesbank was in charge, and Germany maintains persistently large current-account surpluses, which are viewed as evidence that German industry is too competitive. This brings us to the first lesson of the last 20 years: the performance of individual eurozone countries is not preordained.

The experiences of other countries, such as Spain and Ireland, reinforce that lesson, demonstrating that the ability to adapt to changing circumstances and a willingness to make painful choices matter more than the economy’s starting position. This applies to the future as well: Germany’s current predominance, for example, is in no way guaranteed to continue for the next 20 years.

Yet the establishment of the eurozone was backward-looking. The main concern during the 1970s and 1980s had been high and variable inflation, often driven by double-digit wage growth. Financial crises were almost always linked to bouts of inflation, but had previously been limited in scope, because financial markets were smaller and not deeply interconnected.

With the creation of the eurozone, everything changed. Wage pressures abated throughout the developed world. But financial-market activity, especially across borders within the euro area, grew exponentially, after having been repressed for decades. For example, eurozone member countries’ cross-border assets, mostly in the form of bank and other credit, grew from about 100% of GDP in the late 1990s to 400% by 2008.

Then the global financial crisis erupted a decade ago, catching Europe off guard. The first deflationary crisis since the 1930s was made especially virulent in Europe by the mountain of debt that had been accumulated in the previous ten years, when countries had their eyes on the rear-view mirror.

Of course, the eurozone was not alone in being taken by surprise by the financial crisis, which had started in the United States with supposedly safe securities based on subprime mortgages. But the US, with its unified financial (and political) system, was able to overcome the crisis relatively quickly, whereas in the eurozone, a slow-motion cascade of crises befell many member states.

Fortunately, the ECB proved robust. Its leadership recognized the need to shift focus from fighting inflation – the objective the ECB was designed to achieve – to curbing deflation. Ultimately, the euro survived, because, when push came to shove, leaders of the eurozone’s member states expended political capital to implement needed reforms – even after blaming the euro for their countries’ problems.

This pattern of demonizing the euro before recognizing the need to protect it continues to unfold today – and it should serve as a second lesson of the last 20 years. Italy’s populist coalition government used to speak bravely about flouting the euro’s rules, with some advocating an exit from the eurozone altogether. But when financial-market risk premia increased, and Italian savers did not buy their own government’s bonds, the coalition quickly changed its tune.

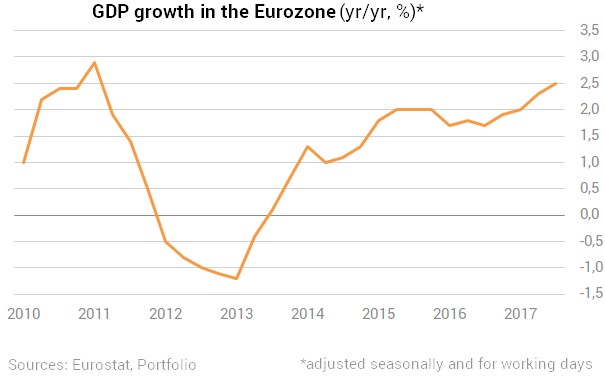

In fact, the eurozone’s economic performance has not been as bad as the seemingly endless stream of bleak headlines implies. Per capita GDP growth has slowed over the last 20 years, but not more so than in the US or other developed economies.

Moreover, continental European labor markets have undergone an under-reported structural improvement, with the labor-force participation rate increasing every year, even during the crisis. Today, a higher proportion of the adult population is economically active in the eurozone than in the US. Employment has reached record highs, and unemployment, though still high in some southern countries, is continuously declining.

These economic realities imply that, even if the euro is not particularly well loved, it is widely recognized as an integral element of European integration. According to the latest Eurobarometer poll, support for the euro is at an all-time high of 74%, while less than 20% of the eurozone’s population opposes it. Even Italy boasts a strong pro-euro majority (68% versus 18%). Herein lies a third key lesson from the euro’s first two decades: despite its many imperfections, the common currency has delivered jobs, and there is little support for abandoning it.

But probably the most important lesson lies elsewhere. The euro’s first 20 years played out very differently than many expected, highlighting the importance of recognizing that the future is likely to be different from the past. Given this, only a commitment to flexibility and a willingness to rise to new challenges will ensure the common currency’s continued success.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Social Protection

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Geographies in DepthSee all

Braz Baracuhy

December 19, 2024