Inflation: What is the best way to measure rising prices?

The Cleveland Fed has developed a median measure, which shows the item in the middle of the range of all price changes every month. Image: Unsplash/ Hulki Okan Tabak

- The Cleveland Fed has developed a median measure, which shows the item in the middle of the range of all price changes every month.

- Even before the pandemic, research found these measures to be less volatile than the traditional core inflation and more closely related to economic slack.

- Similar findings led the Bank of Canada to adopt a weighted median and a trimmed mean as primary measures of core inflation in 2016, replacing their traditional core measure.

Economists debating inflation in the United States are confronting a difficult challenge: stripping out volatile price changes to gauge underlying pressures.

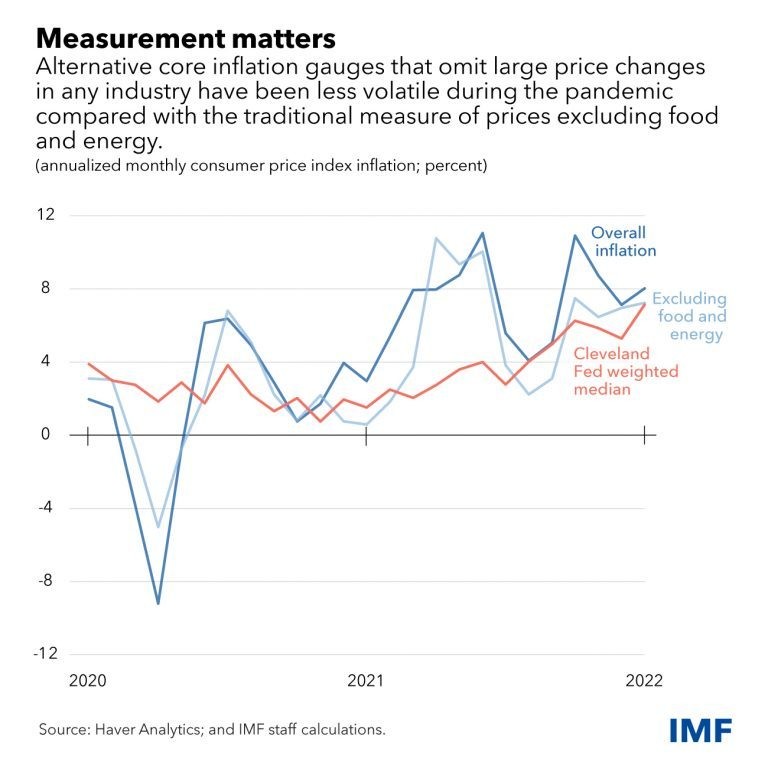

The most common measure of underlying or “core” inflation, which excludes volatile food and energy prices, has been hard to read during the pandemic. The traditional measure came into wider use in the 1970s, when volatile energy prices caused inflation spikes.

Our research shows that for most of the past two years, the traditional core measure was almost as volatile as headline inflation because many large price changes have occurred in sectors outside of food and energy. Examples include airlines, hotels, sporting events, and financial services.

The measures that most successfully filter out transitory movements, we find, are outlier-exclusion measures. Two such gauges developed by regional Federal Reserve banks in Cleveland and Dallas omit large price changes in any industry, and they perform better than gauges that that exclude a fixed set of additional industries, such as the Atlanta Fed’s sticky-price consumer price index.

The Cleveland Fed has developed a median measure, which shows the item in the middle of the range of all price changes every month, while the Dallas bank has a trimmed-mean methodology that omits items in the bottom 24 percent and top 31 percent of the distribution each month. Though slightly different, both filter out most of the monthly fluctuations in headline inflation and have been relatively stable.

They are also more closely related to unemployment and other indicators of economic slack than either headline inflation or the traditional core measure, drifting down when the economy contracted in 2020 and then rising as the economy has rebounded.

These alternative core inflation gauges steadily increased during 2021, confirming that underlying inflation trends in the US have risen.

Just a blip?

Even before the pandemic, research found these measures to be less volatile than the traditional core inflation and more closely related to economic slack.

Over the three decades preceding the pandemic, measures of core that strip out a greater share of outlier price movements were more stable and had a more reliable relationship with unemployment. Inflation excluding food and energy was more volatile than median and trimmed mean inflation and had a much weaker relationship with macroeconomic conditions.

Similar findings led the Bank of Canada to adopt a weighted median and a trimmed mean as primary measures of core inflation in 2016, replacing their traditional core measure.

Overall, we find that the case for the Fed to move away from the traditional measure of core inflation has strengthened during 2020-21.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Global Economic Imbalances

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.