The economic links between China and Latin America

Stay up to date:

Latin America

China is still a distant and exotic country in the mind of many people in Latin America. Yet, with the Asian giant rapidly expanding its ties with the region (the share of exports going to China is now ten times larger than in 2000), their economic fates seem to be increasingly connected. And in fact, a sharper slowdown in China now represents one of the key risks Latin Americans should be worried about—and prepare for. So, what is at stake? How much do shocks to China matter for economies in Latin America?

In an earlier study presented in our April 2014 Regional Economic Outlook, we analyzed growth spillovers in a large model of the global economy, focusing on the link through commodity prices. Here, we complement that analysis by using a simple yet novel approach that exploits the reaction of financial markets to the release of economic data. We find that growth surprises in China have a significant effect on market views about Latin American economies.

Capturing the effects of Chinese shocks through the lens of financial markets

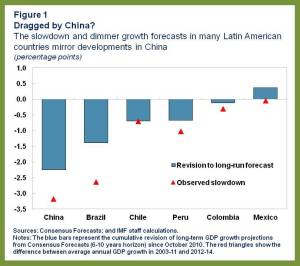

Fast-rising commodity prices in the 2000s, largely fueled by China’s double-digit growth, led to an unprecedented income windfall in many Latin American countries. Against this backdrop, output growth soared from an average of 2.5 percent in 1982-2002 to 4.5 percent in 2003-11. But now the Chinese economy has been slowing, and its long-term projected growth has been cut by 2¼ percentage points since mid-2010 (Figure 1). And something comparable has happened across major economies in Latin America. Are these facts related or do they just reflect a common reaction to something else?

To find out how economic agents reassess the economic prospects for different countries in reaction to surprises about the Chinese economy, we examine the response of FX markets immediately after the release of key economic indicators. The logic is the following. If China matters for the economic prospects of a given country, we would expect its currency to react whenever there is a deviation between the actual outcome and the expected value for that indicator.

Figure 2 shows the response of different exchange rates to a surprise on the growth rate of China’s industrial value added. Indeed, we found that the response of the exchange rates of commodity exporters in Latin America, such as Brazil, Chile and Colombia, are large and significant. (The surprisingly low and insignificant response for the case of Peru could reflect its more frequent exchange rate interventions). The change in JP Morgan’s Latin America currency index is also significant and relatively large (in particular, larger than the change in the analogous Asian currency index). Commodity exporters from other regions, such as Norway, also experience a significant exchange rate response.

The response is strong as well in the case of some other emerging markets, such as Mexico, Poland, and Turkey. While these economies are not highly dependent on commodities, this is not really surprising. Positive news in China tend to lift global confidence and risk appetite, and these are liquid currencies which often act as proxies for other emerging market assets.

Exploring the transmission channels: the role of commodities

With many Latin American countries highly dependent on commodities and China the largest world buyer of these products, the commodity sector must play a key role in the transmission of shocks from China to Latin America. If this is the case, international commodity prices should be affected when activity in China deviates from what the market had expected. Figure 2 (right panel) confirms that, indeed, China’s growth surprises have a significant and large effect on the price of many commodities that are very relevant for Latin America.

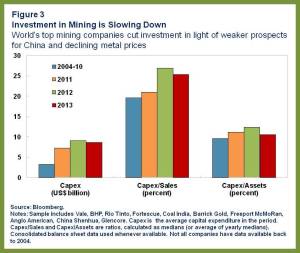

The behavior of investment in the commodity sector is also consistent with the relevance of this channel. Figure 3 shows that capital expenditure by the world’s top mining companies started slowing last year, in a context of revisions to long-term growth in China and declining metal prices. Companies in this sector are now reportedly focused on dealing with structural challenges, such as improving operational efficiency and investment selectiveness.

Preparing for Chinese shocks

A gradual transition to a path of slower and more balanced growth in China is welcome. But shocks to China do matter for Latin America, so the region needs to be prepared forunexpected departures from this smooth transition. Moreover, even if China’s overall slowdown unfolds without bumps, the envisaged rebalancing of its demand, away from commodity-intensive investment and toward consumption, might weaken demand for some commodities, such as metals, by more than currently projected and priced in.

How can the region get prepared? Ensuring prudent fiscal policy, low inflation, and flexible exchange rates, is crucial to increase the resilience of the region to eventual shocks. Beyond macro policies, the region needs to embrace a credible and bold agenda of structural reforms, focusing on improving education, infrastructure, and the business environment. These reforms would boost productivity and the ability to move up the value chain. All of the above would help not only to raise potential growth, but also to reduce the likelihood that negative growth surprises in China would trigger a confidence crisis in Latin America, making the impending adjustment even more difficult.

For an overview of China’s economic and financial relationship with Latin America see also article in Finance and Development.

Published in collaboration with IMF Direct

Author: Bertrand Gruss is an Economist in the Regional Studies Division of the IMF’s Western Hemisphere Department, where he conducts research and analysis on Latin America and the Caribbean.

Image: Rio de Janeiro’s famous “Christ the Redeemer” statue is reflected on the glass facade of a building in Botafogo in Rio de Janeiro February 25, 2011. REUTERS.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Alexis Crow

May 23, 2025

Thelma Obiakor and Bisong Anthony Ekpang

May 23, 2025

Naoko Tochibayashi and Mizuho Ota

May 23, 2025

Jack Hurd and Florian Vernaz

May 21, 2025

Benjamin Wiener

May 21, 2025