How wealth inequality entices talent into finance

Stay up to date:

Financial and Monetary Systems

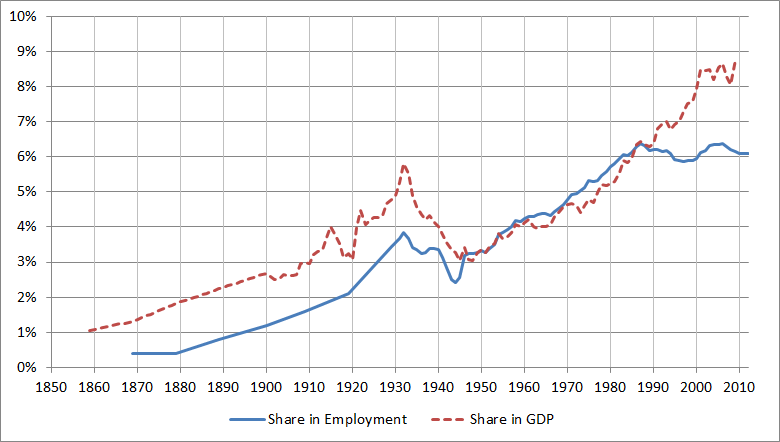

The financial sector has grown steadily and rapidly since World War II in many advanced economies. The growth of the financial sector is apparent by any measure. Figure 1 shows that, particularly in the US, the share of finance in GDP as well as employment has increased substantially. More importantly, the growth of finance has been accompanied by higher relative wages and skill intensity in finance (Philippon and Reshef 2012).

Figure 1. The growth of the US financial sector

The substantial expansion of the financial sector and the increase in relative wages in finance have driven the debate on whether this expansion is socially desirable.

- On the one hand, financial intermediation may be crucial for the efficient allocation of scarce resources.

Merton and Bodie (1995) put it this way: “A well-developed, smooth-functioning financial system facilitates…the efficient allocation of physical capital to its most productive use in the business sector.”

This idea is related to a vast literature arguing that financial development causes economic growth, because by relaxing financial constraints the financial sector corrects capital misallocation and consequently mitigates productivity losses from financial frictions.

- On the other hand, critics of the financial sector suggest that it might have negative implications for the allocation of talent.

James Tobin (1984), stated the issue clearly: “[We] are throwing more and more of our resources, including the cream of our youth, into financial activities remote from the production of goods and services, into activities that generate high private rewards disproportionate to their social productivity”.

Critics of the financial sector have become more vocal in the aftermath of the Global Crisis (Turner 2009, Volcker 2010, Obama 2012). Furthermore, Berkes et al. (2012) provide empirical evidence suggesting that finance starts having a negative effect on output growth when credit to the private sector exceeds 100% of GDP.

The trade-off between efficient capital allocation and entrepreneurship

There is no doubt that the efficient allocation of human as well as physical capital is essential for economic growth. Surprisingly, very few papers have studied the allocation of resources between financial intermediation and final production. Of all available resources, the most valuable is the human mind (talent). In Shakhnov (2014), I attempt to bridge this gap and to evaluate the policy debate in a structured way by building a model in which financial intermediation potentially enhances welfare but draws some talented individuals away from production.

My model is about people who face choices: where to work and where to invest. These people can be talented or not. They can be wealthy or not. I study how these people and their funds should be allocated in the most efficient way. Talent is important for both industry and the financial sector – more talent in industry means more output is produced per unit of capital, while more talent in finance means capital is potentially allocated more efficiently.

The world is not perfect – investors do not where to find a talented entrepreneur, and talented entrepreneurs do not know where to find a wealthy investor. This private information causes the misallocation of capital – talented entrepreneurs receive inefficiently little funding. However, talented bankers can make this distinction – the financial sector can potentially correct this misallocation by matching together a talented entrepreneur and a wealthy investor. The model generates important insights about the financial sector.

- First, the financial sector should be larger for countries or periods with higher wealth and talent inequality, because in these cases the potential productivity losses from capital misallocation are particularly severe.

- Second, the decentralised equilibrium exhibits a misallocation of talent – the financial sector absorbs talent beyond the socially desirable level, because it provides talented agents with an opportunity to extract an excessive informational rent due to the presence of externalities.

When agents make their occupational choice between finance and entrepreneurship, they do not internalise the negative externalities that they impose on investors – the more bankers there are, the fewer talented entrepreneurs and good investment opportunities there are. According to my model, the world is one in which there were too many investment bankers and too few great entrepreneurs. Efficiency can be restored by taxing the financial sector.

Linking wealth inequality and the growth of finance

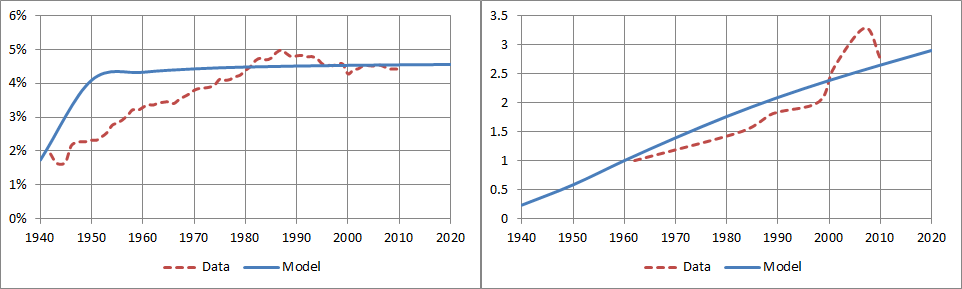

The model provides a novel explanation of the growth of finance by linking it to an increase in wealth inequality. Small initial differences in wealth among investors cause substantial income inequality among entrepreneurs, which is translated into greater wealth inequality next period. The effect is self-reinforcing. Wealthy investors are willing to pay a higher premium for financial services that increase the return on their savings, and so the greater is the dispersion of wealth, the higher is the price of financial services. This higher price induces a larger fraction of talented agents to pursue careers in finance. Hence, the growth of finance and the increase in wealth inequality go hand in hand, as shown in Figure 2.

Figure 2. Share of finance in employment (left panel) and ratio of top 5% wealth to median wealth (right panel)

Note: Data are from the US.

Many studies analyse the causes of the expansion of the financial sector, but none of them connect the expansion of the financial sector and the increase in wealth inequality. I show that the growth of wealth inequality alone is enough to fully explain the growth of finance. This is in line with Piketty and Zucman’s (2014) argument that the primary reason for increased inequality is the fact that financial services associated with asset management generate superior returns, and disproportionately affect the wealthy. According to Greenwood and Scharfstein (2013), much of the growth of the financial sector comes from asset management including private equity, which is mostly a service for wealthy individuals.

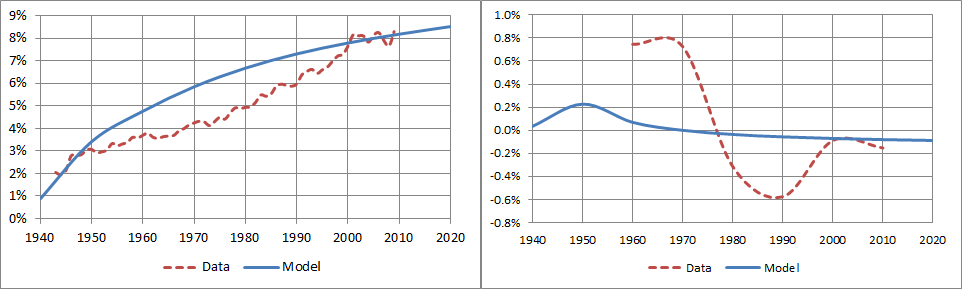

The right panel of Figure 3 shows the US productivity growth has slowed significantly since 1973 with a minor resurgence of productivity in the 1990s. My model links the slowdown to a misallocation of talent. As we can see, the biggest increase in the employment share in finance happened in the 1980s – exactly when we observe the largest drop in the US productivity. In addition, the model predicts that the financial sector would continue to grow as a share of GDP, but not of employment, as we can see by comparing the left panels in Figures 2 and 3. Furthermore, cross-country regressions show that, in line with the predictions of my model, inequalities of wealth and talent are positively associated with the size of the financial sector.

Figure 3. Share of finance in GDP (left panel) and the productivity slowdown (right panel)

Note: Data are from the US.

Policy implications

The issue in my economy is that the return to finance is too high compared to the return to entrepreneurship. Hence an efficient policy should decrease the finance premium, either by taxing bankers or by subsidising startups. Taxation of the financial sector has been a hot topic since the Global Crisis, especially in the EU (see European Commission undated). Subsidies for entrepreneurship are quite common – governments and donors spend billions of dollars subsidising entrepreneurship training programmes around the world (see, for example, European Commission 2013).

Second, in many industrialised countries, banking is a highly concentrated industry and the degree of concentration has been growing. My paper suggests that the increase in the concentration of the financial sector might not be completely undesirable, because one of the implications of my model is that a perfectly competitive financial sector attracts too much talent, while ceteris paribus a monopoly bank would hire fewer bankers. If a monopoly bank could extract the total surplus from intermediation, it would hire the efficient number of bankers.

References

Berkes, E, U Panizza, and J-L Arcand (2012), “Too Much Finance?” IMF Working Paper 12/161, June.

European Commission (2013), “Entrepreneurship Education: A Guide for Educators”, Guide prepared for the European Commission – DG Enterprise and Industry.

European Commission (undated), “Taxation of the financial sector”, webpage, last updated 4 November 2014.

Greenwood, R and D Scharfstein (2013), “The Growth of Finance”, Journal of Economic Perspectives 27(2): 3–28.

Merton, R C and Z Bodie (1995), “A Conceptual Framework for Analyzing the Financial Environment”, in D B Crane, K A Froot, S P Mason, A Perold, R C Merton, Z Bodie, E R Sirri, and P Tufano, The Global Financial System: A Functional Perspective, Boston: Harvard Business School Press: 3–31.

Obama, B (2009), “The President Explains His Larger Vision on the Economy”, Remarks at Georgetown University, 14 April.

Philippon, T and A Reshef (2012), “Wages and Human Capital in the U.S. Finance Industry: 1909–2006”, Quarterly Journal of Economics 127(4): 1551–1609.

Piketty, T and G Zucman (2014), “Capital is Back: Wealth-Income Ratios in Rich Countries, 1700–2010”, Quarterly Journal of Economics, forthcoming.

Shakhnov, K (2014), “The allocation of talent: finance vs. entrepreneurship”, EUI Working Paper ECO 2014/13.

Tobin, J (1984), “On the efficiency of the financial system”, Lloyds Bank Review 153: 1–15.

Turner, A (2009), “How to tame global finance”, Prospect, 27 August.

Volcker, P (2009), “Paul Volcker: Think More Boldly”, Wall Street Journal Future of Finance report, December.

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with Forum:Agenda subscribe to our weekly newsletter.

Author: Kirill Shakhnov is a PhD candidate in Economics at the European University Institute.

Image: A man walks past buildings at the central business district of Singapore February 14, 2007. REUTERS.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Zubaida Bai and Bobbi Gray

May 23, 2025

Respectful national partnerships key to achieving impact and efficiency in international development

Ruth Goodwin-Groen, Pia Bernadette Roman Tayag, Hinjat Shamil and Tidhar Wald

May 5, 2025

Ana Mahony

April 30, 2025

Graham Pearce

April 30, 2025