How does fiscal policy affect growth and stability?

Stay up to date:

Financial and Monetary Systems

A novel approach

To measure whether fiscal policy contributes to stability, the Fiscal Monitor introduces the novel concept of the fiscal stabilization coefficient (FISCO). FISCO measures how much a country’s overall budget balance changes in response to a change in economic slack (as measured by the output gap).

If FISCO is equal to 1 it means that when output falls below potential by 1% of GDP, the overall balance worsens by the same percentage of GDP. The higher the FISCO, the more counter-cyclical is the conduct of fiscal policy, where governments build fiscal buffers in good times that they can then rely on during bad times. The average FISCO among advanced economies is 0.7, with considerable cross-country differences (see figure 1). For the FISCO for individual countries (including advanced, emerging market and developing countries) see Xavier Debrun’s blog “Growth Dividend from Stabilizing Fiscal Policies”.

The FISCO takes into account the fact that many revenue and expenditure items respond to the state of the economy even though the underlying provisions or programs were primarily designed for other reasons. Monitoring the relationship between the budget balance and the output gap would help policymakers understand how much their action contributes to output stability, including in comparison to other countries.

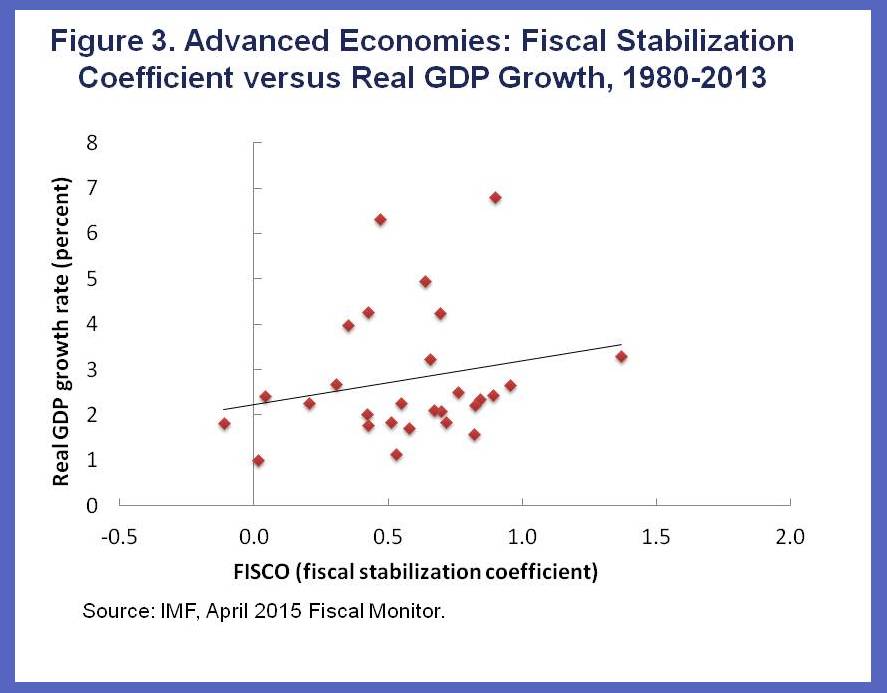

Growth dividends

With the FISCO, the April 2015 Fiscal Monitor assesses the effect that fiscal policy can have on medium-term growth through its support to macroeconomic stability. The findings suggest that countries that can increase their FISCO would be able to significantly reduce macroeconomic volatility (see figure 2).

Why is this important? First, because lower macroeconomic volatility helps avoid wasteful fluctuations in employment and growth. Second, because lower macroeconomic uncertainty provides a favorable environment for physical and social capital, thereby boosting medium-term growth.

Our results show that making fiscal policy more stabilizing would provide a significant boost to growth, as illustrated in figure 3. The effect can be large. Take, for example, the case of an advanced economy that raises its FISCO from the average level (0.7) to that in the top third of countries (about 0.8). This would reduce output volatility by about 15 percent, which in turn brings about a growth dividend of 0.3 percentage points annually. The Fiscal Monitor provides greater details of the methodology underlying this estimate, which attempts to address some of the well-known challenges with growth regressions identified in economic literature. Still, as with all econometric findings, these results must be interpreted with caution.

What this means for countries in practice

What can countries do to improve fiscal stabilization? In an earlier blog (written with Richard Hughes and Laura Jaramillo, Dams and Dikes for Public Finances) we argue that it is crucial to have in place a fiscal framework to manage public finance risks. Well-designed fiscal rules and medium-term frameworks can also help by enabling uninterrupted access to borrowing at favorable conditions, ensuring expenditure control over the entire cycle, and leaving flexibility to respond to output shocks.

Another important aspect of fiscal frameworks is to induce rules-like, automatic stabilizing responses to economic developments. For example, tax payments that move in sync with income, and social transfers, such as unemployment benefits can automatically boost aggregate demand during downturns and moderate it during upswings. Because they operate in real time, without political approval or implementation lags, they are a very effective way to make fiscal policy stabilizing.

This article is published in collaboration with IMF Direct. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with Forum:Agenda subscribe to our weekly newsletter.

Author: Vitor Gaspar, a Portuguese national, is Director of the Fiscal Affairs Department of the International Monetary Fund.

Image: A man walks past buildings at the central business district of Singapore. REUTERS/Nicky Loh.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Khalid Alaamer

April 22, 2025

Jai Shroff

April 22, 2025

Samir Saran and Anirban Sarma

April 17, 2025

Lucia Fry and Naomi Nyamweya

April 17, 2025

Nada AlSaeed

April 16, 2025