Does bank regulation and competition increase transparency?

Stay up to date:

Financial and Monetary Systems

The Global Crisis has brought the ins and outs of bank stability to the attention of increasing numbers of academics and policymakers. But what is the impact of bank regulation and competition on bank opacity? This column presents one of the first evaluations of the impact of bank regulatory reforms on the quality of information disclosed by banks, which in turn helps us assess bank stability.

When banks manipulate their financial statements, this can increase bank opacity and interfere with the private governance and the official regulation of banks. In particular, banks manage their financial statements to smooth earnings, circumvent capital requirements, and reduce taxes. As shown in Beatty and Liao (2011), Bushman and Williams (2012), and Huizinga and Laeven (2012), such manipulations reduce bank stability, the market’s valuation of banks, and loan quality. More generally, the findings by King and Levine (1993) imply that any factor — including earnings management — that interferes with the governance of banks can distort capital allocation and slow growth.

Nonetheless, little is known about the impact of bank regulations and competition on bank opacity. While Morgan (2002) and Flannery et al. (2004) examine the comparative opacity of banks and non-financial firms, they do not examine the determinants of bank opacity. While Barth et al. (2004, 2006, 2009) and Beck et al. (2006) find that banks allocate capital more efficiently in countries that penalise bank executives for disclosing erroneous information, they do not consider the potential role of competition on bank opacity. Given the importance of banks for economic growth, the scarcity of research on the market and regulatory determinants of bank opacity is surprising and consequential.

New research

In new research, we provide the first evaluation of the impact of bank regulatory reforms that spurred competition on the quality of information disclosed by banks (Jiang et al. 2014).

We assess conflicting predictions about the impact of competition on opacity. Models by Alchian (1950) and Stigler (1958) indicate that greater product market competition will compel firms to adopt enhanced corporate governance mechanisms, potentially inducing the disclosure of higher-quality financial statements (e.g. Darrough and Stoughton 1990), to minimise the costs of external finance. An additional line of research suggests that competition can boost the quality of financial statements by facilitating peer-firm comparisons. When firms compete in similar markets, this eases cross-firm comparisons, and the availability of more reliable benchmarks facilitates effective corporate governance, as emphasised by Holmstrom (1982) and Nalebuff and Stiglitz (1983). Indeed, based on a field survey of 169 chief financial officers, Dichev et al. (2013) document that peer-firm comparisons are one of the most important tools for detecting earnings management, and detection is a necessary step in compelling firms to enhance the quality of their financial statements.

In contrast, other models predict that competition increases opacity. In Verrecchia (1983) and Gertner et al. (1988), competition can induce firms to manipulate the flow of information to hinder the entry of potential rivals and gain a strategic advance over existing competitors. In Shleifer (2004), greater competition spurs executives to engage in unethical behaviour, including more aggressive accounting practices.

Regulatory impediments

To evaluate the impact of competition on the quality of information disclosed by banks, we begin by exploiting the removal of regulatory impediments to bank competition among US banks during the last quarter of the 20th century. Interstate bank deregulation eased regulatory impediments to bank holding companies headquartered in one state establishing subsidiaries in other states. These reforms progressed in a time-varying, state-specific process of bilateral and multilateral agreements over two decades that spurred competition among banks, as discussed in Goetz et al. (2013, 2015).

There is, however, an important limitation to these state-time measures of deregulation-induced competition – they do not distinguish among bank subsidiaries, or even bank holding companies within a state. Although interstate bank deregulation spurred competition among banks within the deregulating state, this does not necessarily imply that these regulatory reforms influenced bank opacity by intensifying competition. Perhaps, deregulation triggered, or was associated with, other changes in a state that influenced the quality of information disclosed by banks, and it is these other changes — not increased competition — that influenced bank opacity. To address this concern, we must differentiate among banks within states.

We offer a new approach for constructing time-varying, bank-specific measures of competition. Our approach is based on the ‘gravity model’ view that distance matters for investment and hence for the degree of competition faced by bank subsidiaries and bank holding companies. For example, after state A allows bank holding companies in state B to enter and establish subsidiaries in the state A, two subsidiaries in state A may face different competitive pressures from state B, depending on their distance to state B. That is, when California deregulates with Arizona, the banks in southern California may face greater competitive pressures from Arizona than banks in northern California. By integrating the gravity model with interstate bank deregulation, we build time-varying, bank-specific measures of deregulation-induced competition.

To do this, we first construct measures of the competitive environment facing each subsidiary. For each subsidiary in each time period, we identify those states whose bank holding companies can enter the subsidiary’s state. We then weight each of those states by the inverse of its distance to the subsidiary. This yields an inverse-distance measure of the regulatory-induced competitive environment facing each subsidiary. Second, we calculate the competitive environment facing a consolidated bank holding company by weighting these subsidiary level measures of competition by the proportion of each subsidiary’s assets in the bank holding company.

We then regress various measures of bank opacity on these bank holding company-specific and subsidiary-specific measures of competition while controlling for state-time fixed effects. In this way, we control for all time-varying state characteristics, including the state-time indicators of bank regulatory reforms. By integrating the gravity model into the process of deregulation, we differentiate among the competitive pressures facing banks in the same state and assess whether changes in these competitive pressures influence the quality of their financial statements.

As proxies for bank opacity, we use two strategies for measuring the quality of financial statements. First, we use the frequency with which banks restate their earnings with the Securities and Exchange Commission. Restatements imply that banks misstated their financial statements. Due to data limitations, we can only use financial restatements for a subset of our analyses. The second strategy focuses on loan loss provisions, which are the most important bank accrual through which banks manage earnings and regulatory capital (Beatty and Liao 2014). An extensive literature constructs proxies of the quality of financial statements by estimating a model of loan loss provisions and using the absolute values of the residuals as indicators of discretionary loan loss provisions.

We use a difference-in-differences estimation strategy. The dependent variable is one of the proxies of bank opacity. The core explanatory variables are bank holding company-specific and subsidiary-specific measures of deregulation-induced competition. In these analyses, we not only condition on bank holding company fixed effects and subsidiary fixed effects, respectively, we also condition on state-time fixed effects. Given data availability, we conduct the analyses over the period from 1986 through 2006 using quarterly data.

Discretionary loan loss provisions

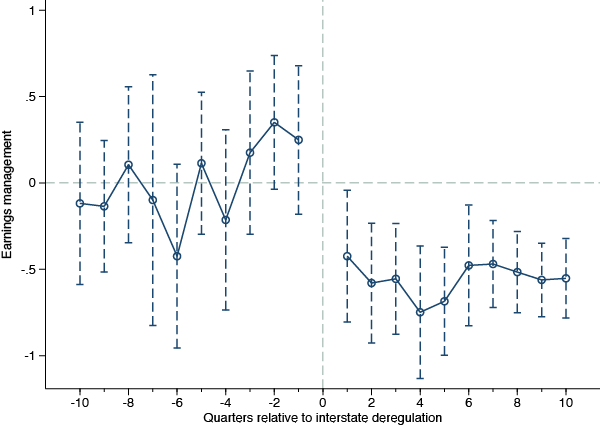

We discover that both the bank holding company-specific and the subsidiary-level measures of regulatory-induced competition are strongly and negatively associated with discretionary loan loss provisions. Figure 1 illustrates this point. Rather than using our approach, which integrates the dynamic process of interstate bank deregulation with the gravity model of market contestability, Figure 1 simply graphs what happens to the discretionary loan loss provisions of banks in state after that state first allows banks from any other state to enter. As shown, discretionary loan loss provisions fall markedly after interstate bank deregulation intensifies competition. The economic magnitudes are substantial. During the pre-deregulation period, the average ratio of discretionary loan loss provisions to bank profits as measured by earnings before taxes and provisions was 28%, but it fell to an average of 13% after regulatory reforms that boosted competition.

Figure 1 Evolution of disclosure quality around interstate bank deregulation

The full estimation results that distinguish among bank holding companies and their subsidiaries yield similarly strong estimates. In these gravity-deregulations analyses, identification comes from differentiating between bank holding companies and subsidiaries within the same state that differ in terms of geographic distances to other states. Thus, the results are not driven by changes in regulatory policies at the state-time level; rather, they are driven by the differential impact of interstate banking reforms on bank holding companies and subsidiaries within a state that arise because of their differential distance to competitors. The findings suggest that interstate bank deregulation reduced discretionary loan loss provisions by intensifying competition.

References

Ahmed, A, C Takeda, and S Thomas (1999), “Bank loan loss provisions: A reexamination of capital management and signaling effects”, Journal of Accounting and Economics 28: 1-25.

Alchian, A (1950), “Uncertainty, evolution, and economic theory”, Journal of Political Economy 58: 211-221.

Barth, J R, G Caprio, and R Levine (2004), “Bank regulation and supervision: What works best?”,Journal of Financial Intermediation 13: 205-248.

Barth, J R, G Caprio, R Levine (2006), Rethinking bank regulation: Till angels govern, Cambridge: Cambridge University Press.

Barth, J R, C Lin, P Lin, F Song (2009), “Corruption in bank lending to firms: Cross-country micro evidence on the beneficial role of competition and information sharing”, Journal of Financial Economics 91: 361-388.

Beatty, A, S Liao (2011), “Do delays in expected loss recognition affect banks’ willingness to lend?”,Journal of Accounting and Economics 52: 1-20.

Beatty, A, S Liao (2014), “Financial accounting in the banking industry: A review of the empirical literature”, Journal of Accounting and Economics 58: 339–383.

Beck, T, A Demirguc-Kunt, R Levine (2006), “Bank Supervision and Corruption in Lending”, Journal of Monetary Economics 53: 2131-2163.

Bushman, R M, C D Williams (2012), “Accounting discretion, loan loss provisioning, and discipline of banks’ risk-taking”, Journal of Accounting and Economics 54: 1-18.

Campbell, T S, W A Kracaw (1980), “Information production, market signaling, and the theory of intermediation”, Journal of Finance 35: 863-882.

Darrough, M, N Stoughton (1990), “Financial disclosure policy in an entry game”, Journal of Accounting and Economics 12: 219-243.

Dichev, I, J Graham, C Harvey, S Rajgopal (2013), “Earnings quality: Evidence from the field”,Journal of Accounting and Economics 56: 1-33.

Flannery, M J, S H Kwan, M Nimalendran (2004), “Market evidence on the opaqueness of banking firms’ assets”, Journal of Financial Economics 71: 419–460.

Gertner, R, R Gibbons, D S Scharfstein (1988), “Simultaneous signaling to the capital and product markets”, Rand Journal of Economics 19: 173–90.

Goetz, M R, L Laeven, R Levine (2013), “Identifying the valuation effects and agency costs of corporate diversification: Evidence from the geographic diversification of U.S. banks”, Review of Financial Studies 26: 1787-1823.

Goetz, M R, Laeven, L, R Levine (2013), “Does the geographic expansion of banks reduce risk?”,Journal of Financial Economics, forthcoming.

Huizanga, H, L Laeven (2012), “Bank valuation and accounting discretion of banks during a financial crisis”, Journal of Financial Economics 106: 614-634.

Jiang, L, R Levine and C Lin (2015), “Competition and Bank Opacity”.

King, R G, R Levine (1993), “Finance and growth: Schumpeter might be right”. Quarterly Journal of Economics 108: 717-738.

Morgan, D P (2002), “Rating banks: risk and uncertainty in an opaque industry”, The American Economic Review 92: 874-888.

Nalebuff, B J, J E Stiglitz (1983), “Information, competition, and markets”, American Economic Review 73, 278-283.

Shleifer, A (2004), “Does competition destroy ethical behavior?”, American Economic Review 94: 414-418.

Stigler, G (1958), “The economies of scale”, Journal of Law and Economics 1: 54-71.

Verrecchia, R (1983), “Discretionary disclosure”, Journal of Accounting and Economics 5: 365-80.

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Authors: Liangliang Jiang is an Associate Professor in Economics, Lingnan University, Hong Kong. Ross Levine is a Professor of Economics at Haas School of Business, University of California at Berkeley. Chen Lin is a Professor in Finance at Department of Finance, Chinese University of Hong Kong.

Image: A sign for Bank Street and high rise offices are pictured in the financial district Canary Wharf in London October 21, 2010. REUTERS/Luke MacGregor.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Swapan Mehra and Akim Daouda

June 16, 2025

Aengus Collins

June 12, 2025

John Letzing

June 11, 2025

Valentina Vellinho Nardin

June 10, 2025

Spencer Feingold

June 10, 2025