How much do financial shocks affect the economy?

Stay up to date:

Financial and Monetary Systems

The experiences of recent years have emphasised the need for a better understanding of the links between the financial sector and the real economy. While substantial effort has been devoted to this topic, many questions remain. One of them is the importance of shocks originating from within the financial sector versus shocks from the real side of the economy to explain fluctuations in economic activity and financial markets.

What has caused the excesses in risk-taking?

Many observers agree that increased risk-taking at banks resulted in excessive lending in the early 2000s, subsequently contributing to the crisis of 2007-2008. However, it is less clear what led to this increased appetite for risk:

- One view is that it was caused by changes in the financial system, such as greater risk-shifting opportunities and the prevalence of skewed incentive schemes (see e.g. Rajan 2005);

- An alternative interpretation is that the risk-taking behaviour of banks was mainly driven by developments external to the banking sector. For example, loose monetary policy has been blamed for providing banks with incentives to take on excessive risk prior to the crisis, the so-called risk-taking channel of monetary policy (e.g. Adrian and Shin 2010; Jiménez et al. 2009; Ioannidou et al. 2009; Maddaloni and Peydró 2011).

What about securitisation markets?

Similarly, there is a broad understanding that securitisation was an important driver of the lending boom prior to the crisis, as well as a major factor contributing to the subprime crisis. Keys et al. (2010) and Purnanandam (2011) have shown that the widespread use of securitisation affected bank behaviour both in terms of amount and quality of loans. Again, it is not clear what triggered the changes in the securitisation markets:

- It may be due to financial innovations which made it easier for banks to transfer risks to investors;

- Securitisation may also have been driven by changes outside securitisation markets, such as shifts in the stance of monetary policy that altered investors’ appetite for risky assets.

Borio and Zhu (2008), for instance, argue that low interest rates lead to a higher appetite and demand for securitisation products by investors, which is often called the search for yield effect of monetary policy. On the other hand, banks typically use securitisation to buffer the effects of monetary policy. In particular, lower interest rates reduce the supply of securitisation by banks because it is cheaper and easier to finance the loans on-balance sheet (Estrella 2002, Loutskina and Strahan 2009, Loutskina 2011).

A clear view on the origin of shocks is needed

Separating shocks which originate in banks and securitisation markets from other shocks is important for understanding how the financial system interacts with the macro-economy. It should help us in assessing the overall role of the financial system in creating as well as amplifying shocks, which is an important input into the design of financial regulation. For example, the scope for regulation is more limited if fluctuations in financial variables mainly arise in response to shocks to the real economy. Furthermore, isolating different types of financial shocks is a prerequisite for studying the macroeconomic consequences of these shocks. Different types of financial shocks may affect output and prices differently, and hence require different policy responses.

Disentangling shocks using a theory-based empirical approach

In a recent paper (Peersman and Wagner 2015) we have analysed the link between the banking sector, securitisation markets and the macro-economy with a structural vector autoregressive model. Relying on a theoretical model of bank risk-taking and securitisation, we identify three types of financial shocks in the structural vector autoregressive model:

- A risk-taking shock alters banks’ cost (real or perceived) of holding risks on their balance sheet. It may arise for instance because banks temporarily underprice (overprice) risk, changes in the risk-shifting incentives of bank managers, or from moral hazard due to variation in bailout expectations;

- A securitization shock makes it more or less attractive for banks to securitise loans. It can be the result, for instance, of financial innovations in securitisation markets relative to a trend of technological progress, or fluctuations in the demand for securitised assets;

- A lending shock is a shock that makes it more profitable for banks to extend loans, for example, because of a change in monitoring costs or because of a shift in the demand for loans which is not caused by developments in the real economy.

Financial shocks are important for the macroeconomy

We estimate the structural vector autoregressive model for the US over the sample period 1970-2008. The results show that the financial shocks are an important source of macroeconomic fluctuations. Together, they account for more than 30% of U.S. output variation.

Financial shocks and their impact on the economy

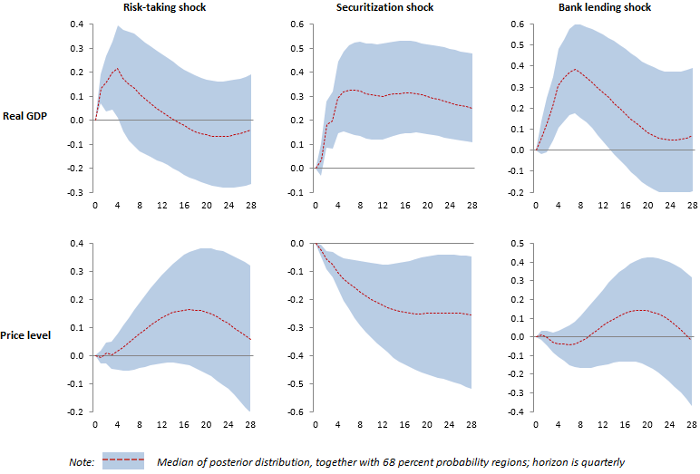

The figure below shows the dynamic effects of the three different types of financial shocks on respectively real GDP and the price level (the figures show the impulse responses of a one-standard deviation exogenous shock in period zero).

Figure 1. Dynamic effects of three different types of financial shocks

The figure reveals that expansionary securitisation shocks lead to a permanent rise in real GDP accompanied by a fall in the price level. In other words, a pattern that is typically found for technology or supply-side shocks. This is consistent with the view that securitisation techniques alleviate financing constraints, and facilitate a more efficient allocation of resources in the economy.

Lending shocks and risk-taking shocks, in contrast, only have a temporary effect on economic activity and they tend to lead to a (moderate) rise in the price level. The pattern of both shocks is hence similar to that of an aggregate demand shock.

Fluctuations in the financial system do not all originate from within the system

An intriguing finding of our analysis is that changes in securitisation and retained loans by banks are predominantly driven by shocks unrelated to securitisation markets and risk-taking. This suggests that a large part of the observed fluctuations in securitization and risk-taking in the data is in fact an endogenous response to developments elsewhere in the economy.

Macroeconomic policies

Given that financial shocks are a significant source of macroeconomic fluctuations, policymakers need to better take into account the role of the financial system. This may imply attempts to reduce the scope for the financial system to be a source of shocks. Current regulatory efforts, in particular aimed at curbing risk-taking at banks and reducing systemic risk in securitisation markets, already go in that direction.

Policymakers also need to take into account the origin of shocks when reacting to fluctuations in the economy. In particular, our results indicate that for the optimal policy response, the source of the shock is critical. For instance, expansionary shocks originating in securitisation markets resemble productivity shocks with deflationary tendencies, while shocks caused by higher risk-appetite, in contrast, tend to lead to higher inflation. On a practical level, this implies that central banks should not only pay attention to changes in total lending in the economy, but should also consider the contribution of banks (loan retention) and markets (securitisation) to such changes.

A cautionary note for policymakers

Our results also provide a cautionary note for interpreting changes in the financial sector too readily. For example, it seems only natural to attribute fluctuations in securitisation to securitisation markets themselves, with implications for financial regulation. However, only a small part of changes in securitisation and risk-taking seems to be caused by shocks to the respective variables themselves. The fluctuations are hence largely a response to developments taking place elsewhere in the economy. This emphasises the need for clearly distinguishing between shocks and endogenous responses in the financial system for policy analysis.

References

Adrian, T and H Shin (2010), “Financial intermediaries and monetary economics”, in B M Friedman and M Wordford (eds.) Handbook of Monetary Economics, Chapter 12: 601-650.

Borio, C and H Zhu (2008), “Capital regulation, risk-taking and monetary policy: a missing link in the transmission mechanism?”, BIS Working Paper Series, 268.

Estrella, A (2002), “Securitization and the efficacy of monetary policy”, Economic Policy Review: 243-255, Federal Reserve Bank of New York.

Ioannidou, V, Ongena, S and J Peydrò (2009), “Monetary policy, risk-taking and pricing: Evidence from a quasi-natural experiment”, manuscript, Tilburg University.

Jiménez, G, Ongena, S, Peydrò J, and J Saurina (2009), “Hazardous times for monetary policy: What do twenty-three million bank loans say about the effects of monetary policy on credit risk-taking?”, Bank of Spain Working Paper Series, 833.

Keys, B, Mukherjee, T, Seru A, and V Vig (2010), “Did securitization lead to lax screening? Evidence from subprime loans”, The Quarterly Journal of Economics 125(1): 307-362.

Loutskina, E (2011), “The role of securitization in bank liquidity and funding management”, Journal of Financial Economics 100: 663-684.

Loutskina, E and P Strahan (2009), “Securitization and the declining impact of bank finance on loan supply: Evidence from mortgage originations”, Journal of Finance 64(2): 861-889.

Maddaloni, A and J Peydro (2011), “Bank risk-taking, securitization, supervision, and low interest rates: Evidence from the Euro area and U.S. lending standards”, Review of Financial Studies 24: 2121-65.

Peersman, G, and W Wagner (2015), “Shocks to bank lending, risk-taking, securitizaton, and their role for U.S. business cycle fluctuations”, CEPR Discussion Paper 10547.

Purnanandam, A (2011), “Originate-to-distribute model and the subprime mortgage crisis”, Review of Financial Studies 24(6): 1881-1915.

Rajan, R (2005), “Has financial development made the world riskier?”, NBER Working Paper No. 11728.

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Gert Peersman is a Professor of Economics at Ghent University (Department of Financial Economics). Wolf Wagner is a Professor of Economics at the University of Tilburg and the Chairman of the European Banking Center.

Image: A view shows the headquarters of a French business in Courbevoie, outside Paris. REUTERS.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Thelma Obiakor and Bisong Anthony Ekpang

May 23, 2025

Naoko Tochibayashi

May 23, 2025

Jack Hurd and Florian Vernaz

May 21, 2025

Benjamin Wiener

May 21, 2025

Alejo Czerwonko

May 20, 2025