How do people in emerging countries feel about their economies?

Stay up to date:

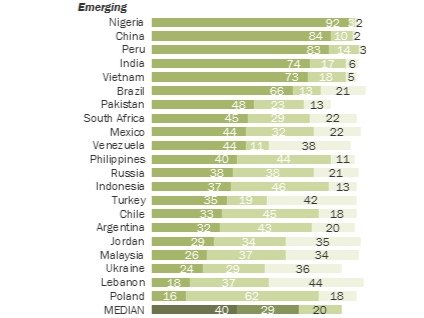

Economic Progress

Chinese citizens have the most confidence in their economy, Nigerians are the most optimistic for the future, and Ukrainians are the most downbeat.

Those are some of the findings from a Pew Research Center study that asked respondents in emerging markets to rate their economy as good or bad.

The study found that overall citizens in emerging and developing markets were more likely to say their economy was good than those in advanced economies.

Business Insider put together a rundown of the research to help make sense of some of the numbers. Here are emerging and developing countries, ordered from highest to lowest percentage of respondents who think their economy is doing well.

Check out the CIA World Factbook — from which each country’s economic background was extracted — here and the full Pew Center Study here.

Chinese respondents were most likely to describe their economy as good, while those in Ukraine were the least likely.

Pew Research Center

Significantly more Russians reported that their economy is doing “bad” than a year ago, with the proportion jumping from 44% in 2014 to 24% in 2015.

Pew Research Center

Lebanese respondents were the most bearish about the future of their economy.

1. China

Who said it’s doing well: 90%, up one point since the previous year, and up 38 points since 2012. Down one percentage point from 2010.

Who said the economy will improve: 84%, up four points since 2014 and down three points from the country’s all time high in 2010.

What’s going on with the country: The country’s GDP failed to hit its target in 2014, and at 7.4 percent in 2014, growth is slowing. The Chinese markets have crashed in recent months, with the drop starting in June, a little after this survey was conducted. The Chinese government is on a hunt to find those responsible for the crash, while analysts are comparing the crash to the dot-com bubble or the Black Tuesday crash in 1929. (CIA world Factbook)

GDP: $10.3 trillion in 2014 with 7.4% growth (World Bank)

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Julia Hakspiel

June 17, 2025

Swapan Mehra and Akim Daouda

June 16, 2025

Aengus Collins

June 12, 2025

John Letzing

June 11, 2025

Valentina Vellinho Nardin

June 10, 2025

Spencer Feingold

June 10, 2025