How can Europe raise its competitiveness?

Stay up to date:

European Union

Eight years since the onset of the financial crisis, Europe is still struggling to reignite its growth engine: while growth in the European Union is projected to pick up this year to 1.8%, compared with 1.4 % in 2014, overall growth rates remain subdued beyond the duration of a typical business cycle. At the same time, unemployment is persistently high – above 10% in many of the hardest-hit economies. The same holds true for productivity growth, which has been growing more slowly in Europe than in other regions.

What explains this slowdown? The findings of the Global Competitiveness Report 2015-2016 provide some indicators.

If Europe is to chart a course for solid growth, it will have to face, embrace and leverage current changes in the global economy: a move away from traditional manufacturing towards entirely new consumption models and industries. Staying ahead in this so-called “industry 4.0” context is paramount for Europe, a region where industry generates 80% of innovation, 75% of exports and 25% of private sector jobs.

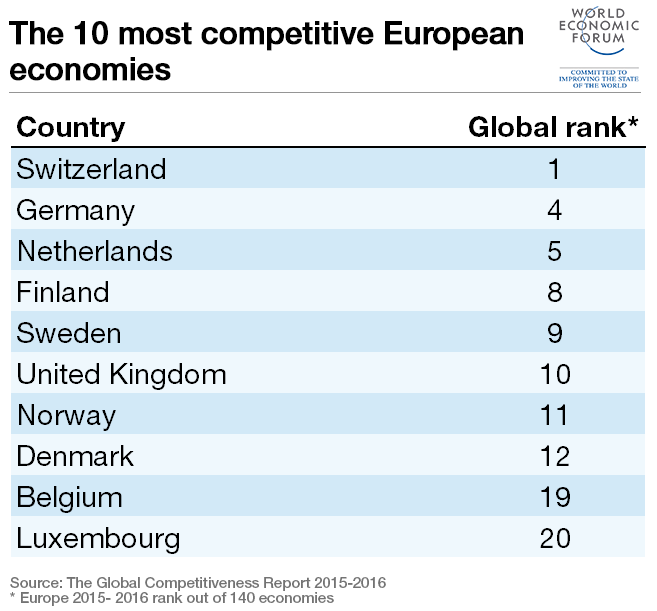

At first glance, EU economies appear well poised to do so: half of the world’s 20 most innovative economies are from the region, and overall there is a solid and rapid ICT uptake across Europe, ranging from Luxembourg (1st globally) to Hungary (48th). But for two reasons, there is no room for complacency.

First, there is a huge difference across the region in terms of how well countries performed in the innovation pillar. While many northern and north-western European countries are among the worlds’ most innovative economies – such as Finland (2nd), Germany (6th) and the Netherlands (8th) – the majority of central and eastern European, and to some extent southern European economies, are significantly trailing behind, with Bulgaria (94th) coming last in the region. This is worrying for those central and eastern European economies with a traditionally high share of manufacturing, such as the Slovak Republic, Romania and Hungary. Only Slovenia (33rd) and the Czech Republic (35th) scored well.

Second, to stay ahead of the curve in a fast-paced and fast-changing global economy, countries must remain agile and flexible in the face of changing demands. Talent is the best way of doing that. Looking back over the past decade, this year’s Global Competitiveness Report shows that countries that identify, nurture, use and reward talent tend to be more competitive. For that reason, they also appear to withstand crises better or to recover more swiftly.

Projecting this into the future, talent-driven economies will have a higher chance of navigating the new terrain. Even in many of the region’s most competitive economies, good education systems and efficient use of talent are both thwarted by significant labour market rigidities. This is the case in Finland, Germany and Belgium (all ranking below 100 when it comes to labour market flexibility). Only the UK, Denmark and Ireland marry both a top-notch education system with the ability to allocate talent to its most productive uses. At the same time, access to finance – particularly for small and medium-sized enterprises – remains a common threat to all countries and is the region’s greatest impediment to creating a knowledge-driven economy.

Talent will help Europe escape its “new normal” of subdued growth, high unemployment and low productivity, while laying the foundations for sustained future growth in a highly uncertain and changing environment. The risk, however, lies in the transition – prolonged high unemployment rates have left many parts of the labour force without the skills they need, particularly in southern Europe.

This could lead to a generation of Europeans unhappy and disillusioned with the European project, as we’re already starting to see with the increasing popularity of populist parties. But while some might be tempted to withdraw back into their borders, this is at odds with a globalized future driven by knowledge and innovation. Enhancing competitiveness in Europe will therefore start with the recognition that Europe’s sum is more than its parts, as well as a commitment from all stakeholders to seeing through often difficult trade-offs.

The Global Competitiveness Report 2015-2016 is available here.

Have you read?

The world’s top 10 most competitive economies

The top 10 most competitive economies in Europe

Author: Caroline Galvan, Economist, Global Competitiveness and Risks, World Economic Forum

Image: Visitors take pictures as they are lifted in a glass gondola to the top of the Globe Arena in Sweden’s capital Stockholm May 1, 2013. REUTERS/Arnd Wiegmann

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Aengus Collins

April 15, 2025

Spencer Feingold

April 15, 2025

Andrew Collinge and Katie Adnams

April 11, 2025

John Letzing

April 11, 2025

Michelle You

April 10, 2025

Steve Reis and Jill Zucker

April 10, 2025