How can we better predict economic risks?

Stay up to date:

Global Governance

The Global Crisis and its high economic costs have revived the academic and policy interest in ‘early warning indicators’ to provide timely alert of economic risks (e.g. Rose and Spiegel 2011, Alessi and Detken 2011). In our recent paper (Röhn et al. 2015), we take stock of the voluminous early warning literature on currency, banking, and sovereign debt crises, and of recent research on the Global Crisis. We discuss the source and nature of potential vulnerabilities that can lead to costly economic crises in OECD countries. Drawing lessons from the literature review, we build a new dataset of more than 70 indicators assembled from a number of public data sources that could be monitored to detect vulnerabilities and assess country risks of suffering a crisis. The dataset covers, to the extent possible, the 34 OECD economies, the BRIICS (Brazil, Russian Federation, India, Indonesia, China, and South Africa), Colombia, and Latvia. The database is accessible at the Economic Resilience Website.1

In Hermansen and Röhn (2015), we then go one step further and use the dataset to assess how useful the indicators would have been in signalling the severe recessions and crises that hit the 34 OECD economies and Latvia between 1970 and 2014. The empirical analysis shows that the majority of the proposed indicators would have signalled well in advance the severe recessions and crises that occurred in OECD countries during the last 40 years.

A bird’s eye view of the areas covered by the indicators

The dataset contains indicators grouped into six areas: financial sector imbalances; non-financial sector imbalances; asset market imbalances; public sector imbalances; external sector imbalances; and spillovers, contagion, and global risks.

Figure 1 gives a stylised description of the vulnerabilities covered and illustrates some of the channels through which vulnerabilities build-up. A detailed narrative of the source and nature of potential vulnerabilities is given in Röhn et al. (2015).

Figure 1. A stylised description of the areas covered by the vulnerability indicators

Source: Röhn et al. (2015).

- Financial sector imbalances

These include indicators in three main categories. The first category refers to leverage and excessive risk taking of the financial sector. It includes indicators such as leverage, capital ratios, and lending standards. A second category aims at capturing liquidity and currency mismatches which increase liquidity risk. It includes indicators of ratios of liquid assets to short-term liabilities, loan-to-deposit ratios, and the net open foreign currency position of the financial sector. The final category includes information on common exposures of banks to, for example, sovereigns or the housing market.

- Non-financial sector imbalances

The focus is mainly on vulnerabilities stemming from balance sheet imbalances of households and non-financial corporations that may result in financial instability. The indicators cover different measures of credit and credit growth to households and non-financial corporations as well as measures of liabilities for households and non-financial corporations (e.g. gross financial, foreign currency denominated, and short-term liabilities).

- Asset market imbalances

Indicators of asset market imbalances mainly relate to housing market and equity market misalignments. Indicators include real house prices and ratios of house prices to disposable income and rents, as well as real stock prices. Besides interlinkages with private sector balance sheets, house price booms can affect the real economy if they are associated with booms in residential investment, as experienced in several European countries prior to the Crisis. To capture this housing market-real economy nexus, the dataset includes the share of residential investment in GDP and the share of employment in construction.

- Public sector imbalances

The indicators of public sector imbalances mainly relate to sovereign solvency risk, including basic fiscal solvency, long-term fiscal solvency indicators, and government debt composition indicators. Indicators measuring basic solvency risk include the primary budget balance, the general government debt and the differential between the sovereign bond yield and potential GDP growth rate differential. Long-term fiscal solvency indicators include future public spending in pensions and health, as well as the projected age dependency ratio.

- External imbalances

The external imbalances indicators include the current-account balance, external debt, FDI liabilities, currency mismatch, external reserves, and the real effective exchange rate.

- International spillovers, contagion, and global risks

A key insight from the 2008/09 Crisis was that even countries without significant domestic imbalances were affected by the Crisis through international spillovers and contagion. Indicators of trade and financial openness are included to account for vulnerabilities to international spillovers. Indicators of global risks are also included. They are constructed as GDP-weighted averages of country-specific imbalances.

Vulnerabilities in each of the five domestic areas should not be taken in isolation. Indeed, in the boom phase of the business cycle many of the imbalances interact and can reinforce each other. In the bust phase, the unwinding of one imbalance can trigger the unwinding of others, as we discuss in detail in Röhn et al. (2015). The simultaneous unwinding of several imbalances will often exacerbate the downturn and deepen the crisis. Conversely, if policymakers tackle one imbalance, they are also likely to reduce vulnerabilities in other sectors.

Are the vulnerability indicators useful?

In Hermansen and Röhn (2015), the usefulness of the vulnerability indicators for which we have sufficiently long time series is evaluated applying a methodology commonly used in the early warning literature, the signalling approach (Kaminsky et al. 1998). According to this approach, an indicator signals a future costly economic event if it crosses a threshold. Threshold levels are set by minimising a loss function, which balances two types of errors: missing crises (so called type I errors), and false alarms (so called type II errors). The errors are weighted by policymakers’ preferences for each type of error. An indicator is then considered as useful if the associated loss is lower than a benchmark case in which the indicator is disregarded.

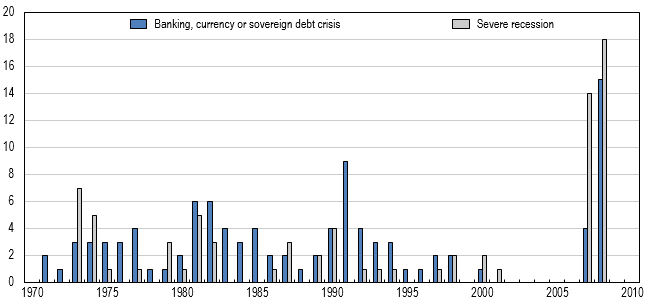

A novelty of the analysis is that we use severe recessions as a measure of costly economic events, in contrast to most of the early warning literature, which has typically focused on particular types of economic crises, such as currency, banking crises, and more recently, broader systemic financial events. Severe recessions provide an efficient and transparent way to capture a wide range of costly economic events and overcome the difficulty of identifying economic crises in an objective way. It is also an outcome that policymakers are presumably most concerned to avoid. We define severe recessions as those with a fall in GDP per capita from peak to trough above 3.5 % of peak GDP per capita (the mean GDP per capita fall in our sample). As Figure 2 shows, crises and severe recession dates do not always coincide. In particular, the severe recession measure identifies many more countries that suffered during the Global Crisis than the defined crises indicators.

Figure 2. Severe recessions and crises dates

Source: Crisis data are taken from Babecký et al. (2012) and authors ‘calculations for severe recessions.

The majority of indicators appear to be useful early warning indicators for severe recessions when policymakers are strongly averse to missing severe recessions, i.e. they are willing to accept a higher rate of false alarms so as to limit the risk of missing an upcoming severe recession. What is perhaps more important from a policy perspective is that most indicators issue first warning signals with sufficient time for policymakers to react, on average, more than 1.5 years before the onset of a severe recession. However, the extent of the signalling power varies across indicators and the results are sensitive to the exact specification of policymakers’ preferences between missing crises and false alarms.

Indicators of global risks are relatively more useful than domestic indicators in signalling severe recessions. In particular, measures of a global credit-to-GDP ratio (growth and gaps from a trend), a global equity price gap, and a global house price gap perform particularly well both in sample and out-of sample. This finding highlights the importance of taking international developments into account when assessing domestic vulnerabilities.

In the domestic areas, indicators that measure asset market imbalances (real house and equity prices, house price-to-income, and house price-to-rent), also perform consistently well both in and out-of sample. Domestic credit related variables appear particularly useful in signalling upcoming banking crises and in predicting the Global Crisis out-of-sample. Indicators of external imbalances such as current-account balances, official reserves, and foreign currency exposure perform well in certain specifications.

Conclusions and lessons for policy

Vulnerability indicators can be a valuable input for monitoring economic risks and our work provides an additional tool for monitoring risks in OECD countries. Indicators are no silver bullet, though. As our research shows, there are limitations when it comes to their predictive power. Vulnerability indicators should be complemented with other monitoring tools and in-depths assessments, including expert judgement, to provide a holistic assessment of country risks.

Authors’ note: The opinions expressed in this column are those of the authors and do not necessarily reflect the views of the OECD.

References

Ahrend, R and A Goujard (2012), “International Capital Mobility and Financial Fragility – Part 1. Drivers of Systemic Banking Crises: The Role of Bank-Balance-Sheet Contagion and Financial Account Structure”, OECD Economics Department Working Papers, No. 902, OECD Publishing.

Alessi, L and C Detken (2011), “Quasi real time early warning indicators for costly asset price boom/bust cycles: A role for global liquidity”, European Journal of Political Economy, Vol. 27/3, pp. 520-533.

Borio, C and M Drehmann (2009), “Assessing the Risk of Banking Crises – Revisited”, BIS Quarterly Review, March 2009, pp. 29-46.

Corsetti, G, K Kuester, A Meier, and G Mueller (2012), “Sovereign Risk, Fiscal Policy, and Macroeconomic Stability”, IMF Working Paper, WP/12/33.

Csortos, O and Z Szalai (2014), “Early warning indicators: financial and macroeconomic imbalances in Central and Eastern European countries”, MNB Working Papers, Vol. 2014/ 2, Magyar Nemzeti Bank.

Frankel, J and G Saravelos (2012), “Can leading indicators assess country vulnerability? Evidence from the 2008–09 global financial crisis”, Journal of International Economics, Vol. 87/2, pp.216-231.

Hermansen, M and O Röhn (2015), “Resilience: The Usefulness of Early Warning Indicators in OECD Countries”,OECD Economics Department Working Papers, No. 150, OECD Publishing.

Jordà, O, M Schularick and A Taylor (2010), “Financial Crises, Credit Booms, and External Imbalances: 140 Years of Lessons”, NBER Working Paper Series, No. 16567.

Kaminsky, G, S Lizondo and C Reinhart (1998), “Leading Indicators of Currency Crises”, IMF Staff Papers, Vol. 45, No. 1,

Lo Duca, M and T Peltonen (2013), “Assessing Systemic Risks and Predicting Systemic Events”,Journal of Banking & Finance, Vol. 37/7, pp. 2183-2195.

Röhn, O, A Caldera Sánchez, M Hermansen and M Rasmussen (2015), “Economic Resilience: A New Set of Vulnerability Indicators for OECD Countries”, OECD Economics Department Working Papers, No. 149, OECD Publishing.

Rose, A, and M Spiegel (2011), “Cross-country Causes and Consequences of the Crisis: An Update”, Special Issue: Advances in International Macroeconomics: Lessons from the Crisis,European Economic Review, Vol. 55/3, pp. 309–324.

Schularick, M and A Taylor (2012), “Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008”, American Economic Review, 102, No. 2, pp. 1029-61.

Sutherland, D and P Hoeller (2012), “Debt and Macroeconomic Stability: An Overview of the Literature and Some Empirics”, OECD Economics Department Working Papers, No. 1006, OECD Publishing.

Footnote

1 Information and links to the database containing the indicators can be found in the Economic Resilience Website: http://www.oecd.org/economy/growth/economic-resilience.htm .

This article is published in collaboration with [was first published by] VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Aida Caldera is a Senior Economist in the OECD Economics Department. Mikkel Hermansen and Oliver Röhn are Economists in the OECD Economics Department.

Image: A worker arrives at his office in the Canary Wharf business district in London February 26, 2014. REUTERS/Eddie Keogh.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Equity, Diversity and InclusionSee all

Silja Baller

May 15, 2025

Tea Trumbic and Dhivya O’Connor

May 13, 2025

Harrison Lung and Hatem Bamatraf

May 7, 2025

Zainab Azizi

April 9, 2025