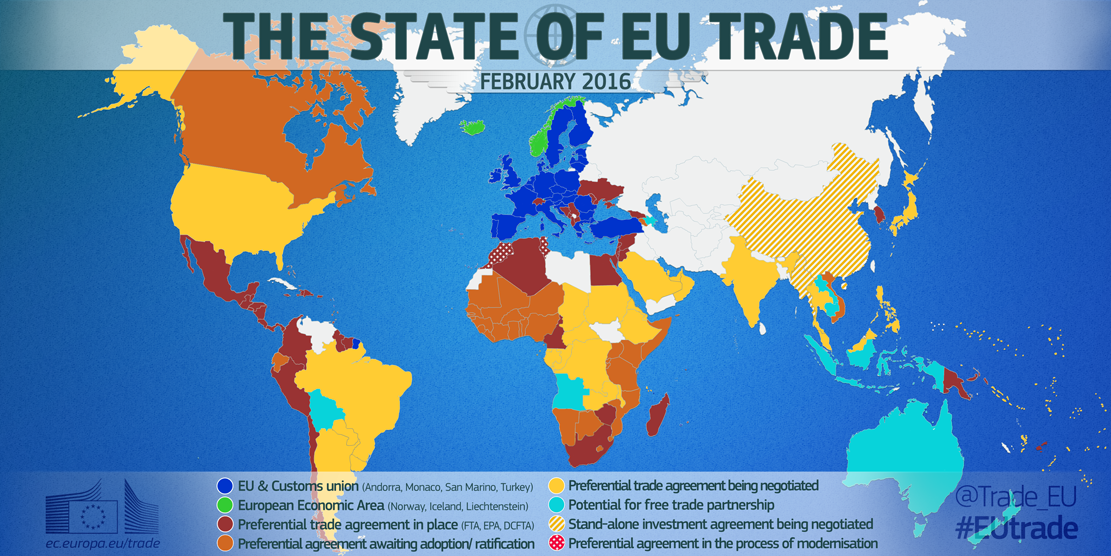

The world’s free trade areas – and all you need to know about them

NAFTA, TTIP, MERCOSUR, FTA ... the acronym-rich world of free trade explained

Image: REUTERS/Paulo Whitaker

Stay up to date:

Trade and Investment

International trade is a driving force behind economic growth, and two so-called “mega-regional” trade deals are dominating public debate on the issue: the Trans-Pacific Partnership (TPP) and the Transatlantic Trade and Investment Partnership (TTIP).

But there are around 420 regional trade agreements already in force around the world, according to the World Trade Organization. Although not all are free trade agreements (FTAs), they still shape global trade as we know it.

What exactly are free trade areas?

The OECD defines a free trade area as a group of “countries within which tariffs and non-tariff trade barriers between the members are generally abolished but with no common trade policy toward non-members”.

The free movement of goods and services, both in the sense of geography and price, is the foundation of these trading agreements. However, tariffs are not necessarily completely abolished for all products.

Which are the world’s major free trade areas?

- The North American Free Trade Agreement (NAFTA)

Free trade between the three member nations, Canada, the US and Mexico, has been in place since January 1994. Although tariffs weren’t fully abolished until 2008, by 2014 total trilateral merchandise trade exceeded US$1.12 trillion.

According to the US government, trade with Canada and Mexico supports more than 140,000 small and medium-size businesses and over 3 million jobs in the US. Gains in Canada are reportedly even higher, with 4.7 million new jobs added since 1993. The country is also the largest exporter of goods to the US.

However, the Council on Foreign Relations suggests that the impact on Mexico is harder to assess. Per capita income has not risen as fast as expected; nor has it slowed Mexican emigration to the US. However, farm exports to the US have tripled since 1994, and the cost of goods in Mexico has declined. The cost of basic household goods has halved since NAFTA came into force, according to estimates by GEA, a Mexican economic consulting firm.

Association of Southeast Asian Nations Free Trade Area (AFTA)

The AFTA was signed in January 1992 in Singapore. The original members were Brunei, Indonesia, Malaysia, Philippines, Singapore and Thailand. Four countries have subsequently joined: Vietnam, Laos, Myanmar and Cambodia.

The bloc has largely removed all export and import duties on items traded between the nations. It has also entered into agreements with a number of other nations, including China, eliminating tariffs on around 90% of imported goods.

The AFTA nations had a combined GDP of US$2.3 trillion in 2012, and they're home to 600 million people. The agreement has therefore helped to dramatically reduce the cost of trade for a huge number of businesses and people.

Southern Common Market (MERCOSUR)

Although MERCOSUR was envisaged as a Latin American single market, enabling the free movement of people, goods, capitals and services, this vision is yet to become reality. Internal disputes have slowed progress towards removing tariffs and the free movement of people and goods.

But MERCOSUR is still one of the world’s leading economic blocs, and has a major influence on South American trade and the global economy.

Common Market of Eastern and Southern Africa (COMESA)

Formed in December 1994, the organization aims to develop natural and human resources to benefit the region’s population. Its primary focus, according to the United Nations, is to establish a large economic and unit to overcome barriers to trade.

With 19 member states, and an annual export bill in excess of $80 billion, the organization is a significant market place, both within Africa and globally.

COMESA utlimately aims to remove all barriers to intra-regional trade, starting with preferential tariffs and working towards a tariff-free common market and economic union.

What about the European Union?

The EU is a single market, which is similar to a free trade area in that it has no tariffs, quotas or taxes on trade; but a single market allows the free movement of goods, services, capital and people.

The EU strives to remove non-tariff barriers to trade by applying the same rules and regulations to all of its member states. The region-wide regulations on everything from working hours to packaging are an attempt to create a level playing field. This is not necessarily the case in a free trade area.

The creation of the single market was a slow process. In 1957, the Treaty of Rome established the European Economic Community (EEC) or Common Market. However, it was not until 1986 that the Single European Act was signed. This treaty formed the basis of the single market as we know it, as it aimed to establish the free-flow of trade across EU borders. By 1993 this process was largely complete, although work on a single market for services is still ongoing.

Today, the EU is the world’s largest economy, and the biggest exporter and importer. The EU itself has free trade agreements with other nations, including South Korea, Mexico and South Africa.

What about the TPP and TTIP?

Once fully ratified, the Trans-Pacific Partnership is set to become the world’s largest trade agreement. The TPP already covers 40% of global GDP, and trade between member nations is already significant.

However, by removing tariffs and other barriers to trade, the agreement hopes to further develop economic ties and boost economic growth.

The Transatlantic Trade and Investment Partnership is a deal currently being negotiated between the EU and the US. If reached, it would itself become the world’s largest trade agreement – covering 45% of global GDP.

Like the TPP, it aims to cut tariffs and regulatory barriers to trade. Among these is the removal of customs duties, according to the EU's negotiation factsheet.

The Center for Economic Policy Research has estimated that the deal would be worth $134 billion a year for the EU and $107 billion for the US – although opponents have disputed these figures.

As the World Economic Forum’s E15 Initiative has highlighted, effective global trade is central to economic growth and development. Trade agreements are an integral part of making this a reality.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Trade and InvestmentSee all

Kao Kim Hourn

May 26, 2025

Zhou Weihuan and Stephen Olson

May 26, 2025

Alexis Crow

May 23, 2025

Thelma Obiakor and Bisong Anthony Ekpang

May 23, 2025

Boyang Xue

May 21, 2025