What a decline in manufacturing jobs means for developing economies

Manufacturing jobs have seen a steady decline in advanced economies over recent decades.

Image: REUTERS/James Pomfret

Stay up to date:

Artificial Intelligence

Manufacturing employment has seen major shifts over the past several decades. The share of manufacturing in aggregate employment has been steadily declining for over four decades in advanced economies (Figure 1), with most countries experiencing outright declines in the number of manufacturing jobs since the 1990s. In most developing economies, the share of manufacturing jobs has levelled off at relatively low levels as labour has shifted from agriculture to services, largely bypassing the manufacturing sector. The main exceptions have been China, Indonesia, Malaysia, and Thailand, where the share of manufacturing jobs in overall employment is higher than in the 1970s.

Figure 1 Manufacturing employment share

Note: The solid lines and shaded areas denote the simple average and the interquartile range across economies, respectively.

These trends have concerned policymakers and the broader public alike. In advanced economies, the worry is that middle-skilled workers displaced from manufacturing jobs may need to accept lower-paid jobs that require less skills in the service sector, with a ‘hollowing out’ of the income distribution and rising inequality. In developing economies, the concern is that skipping a traditional industrialization phase may harm productivity growth and income convergence toward advanced economies (Rodrik 2016).

In a recent IMF report we revisit the implications of changing manufacturing employment shares for economy-wide productivity and income inequality (IMF 2018). Our findings suggest that services, like manufacturing, can potentially drive economy-wide productivity growth, and that the decline in manufacturing jobs has contributed little to the rise in labour income inequality in advanced economies.

But policies have a key role to play. Reducing barriers to entry and trade in services and bolstering work-force skills would help ensure that the expansion of the productively dynamic service sectors is not constrained by domestic demand and skill shortages. And facilitating the reskilling of displaced workers and strengthening safety nets is crucial to alleviate the negative consequences of disappearing manufacturing jobs.

Manufacturing and per capita income growth

Historically, the growth of economy-wide productivity appeared to slow once factors of production begin to shift from manufacturing to services (Baumol 1967). And there is evidence that manufacturing can catalyse income convergence across countries, as labour productivity in manufacturing tends to converge to the global technological frontier (Rodrik 2013) – that is, to grow faster in those countries where it is relatively low. Indeed, a strong expansion of manufacturing employment and exports helped countries like Korea achieve significant income convergence towards high-income countries in the past (Jones and Olken 2005, Johnson et al. 2007).

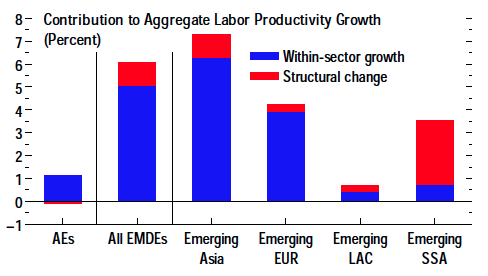

But non-manufacturing activities are very diverse, so the relevant question is whether some service sectors exhibit productivity convergence as well. In IMF (2018), we confirm that productivity growth among services industries in a wide set of advanced and developing countries ranges from the slowest to the fastest in the economy (as documented, for instance, in Baumol et al. 1985 and Jorgenson and Timmer 2011). Moreover, we find that the level of labour productivity in some market service sectors is comparable to or higher than in manufacturing as a whole.1 Following the approach in Diao et al. (2017), we then show that structural change since the early 2000s was growth-enhancing for developing countries.2 That is, the shift of workers from agriculture to services has tended to raise economy-wide productivity (Figure 2).

We also assess whether unconditional productivity convergence across countries – that is, convergence regardless of policies, institutions, and other country characteristics – is unique to the manufacturing sector. Using data for 19 advanced and 20 developing economies between 1965 and 2015, we follow the approach in Bernard and Jones (1996) to test whether labour productivity growth in each of nine market sectors is faster when the initial gap between its productivity level and that at the technological frontier is larger.

Figure 2 Structural change and aggregate labour productivity growth, 2000–2010

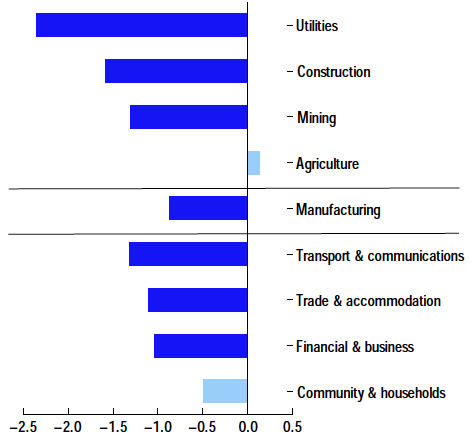

The results confirm that Rodrik’s (2013) finding of unconditional productivity convergence in manufacturing also holds in our sample. But they also show evidence of unconditional convergence in several market service industries (as implied by the negative reading of the solid blue bars in Figure 3). Ancillary evidence suggests that the extent of convergence in services has increased since the mid-1990s or early 2000s, a period when tradability in services expanded.

Interestingly, there is no evidence of productivity convergence in agriculture. Given the size of the sector in low-income countries, this may explain why it has been typically difficult to find evidence of unconditional convergence in economy-wide income per worker (e.g. Rodrik 2013).

Figure 3 Unconditional sectoral productivity beta-convergence estimates

Note: The bars denote the estimated coefficients from sectoral beta-convergence regressions––that is, regressions of labor productivity growth in each sector on its initial level, relative to that in the US. A solid bar denotes that the coefficient is statistically significant at the 95 percent level.

Manufacturing and income inequality

Manufacturing industries have been a major source of high-quality jobs for medium- to low-skilled workers (see evidence for the US in Helper et al. 2012). The loss of manufacturing jobs as factories close in advanced economies has thus fuelled concerns about the distribution of labour income.

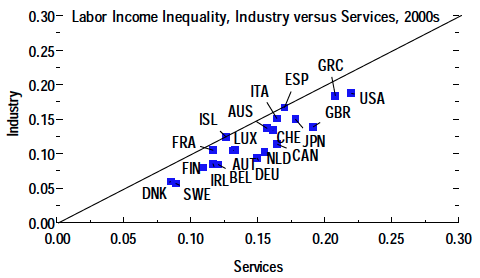

In IMF (2018) we use household- and worker-level data from household surveys in 20 advanced economies to compare the level and distribution of labour earnings in services versus industry (two-thirds of which is accounted by manufacturing), and to assess the extent to which the decline in the share of manufacturing jobs may explain changes in aggregate labour inequality.

Our constructed measures of labour income within each sector indicate that pay in industry is somewhat higher and more evenly distributed than in the service sector.3 But there is high correlation between inequality in both sectors – if a country has high earnings inequality is services, it tends to have high inequality in industry as well (Figure 4, top panel).

Figure 4 Labour income inequality

Moreover, a set of decomposition exercises suggest that the changes in aggregate inequality in advanced economies since the 1980s are mostly accounted by changes in earnings inequality within sectors, rather than by shifting shares of employment between them. Countries that experienced a relatively large increase in economy-wide labour income inequality also tended to register substantial increases in within-sector inequality (Figure 4, bottom panel). Our calculations suggest that, on average, only about one-tenth of the overall increase in inequality between the 1980s and the 2000s can be attributed to the decline in the share of manufacturing jobs.

Conclusion and policy implications

Our findings suggest that a relative decline of manufacturing employment should not necessarily hurt the income convergence prospects of developing economies. But income growth and convergence are not guaranteed to take place on their own either. The pace of growth of domestic demand or the availability of workforce skills can constrain the expansion of the productively dynamic service sectors. To ensure that domestic demand does not constrain service-led growth, enhancing the tradability of services by reducing domestic barriers to entry and barriers to international services trade would be beneficial. Policy should also ensure that the workforce skills are aligned with those needed in sectors enjoying higher productivity. Another key takeaway is that the goal of supporting equitable growth would be better served by efforts to raise productivity in all sectors, rather than on supporting the flow of resources into the manufacturing sector.

Even if the loss of manufacturing jobs in advanced economies may have contributed relatively little to aggregate inequality in advanced economies, the negative consequences appear to have been sizable and persistent for some groups of workers and their communities. Expanding access to programmes that facilitate the reskilling of displaced workers and reduce the costs of their reallocation, as well as strengthening safety nets and targeted redistribution policies, can help soften the blow imposed by structural transformation and help ensure that the gains of productivity growth are shared more broadly.

Authors’ note: This column draws from Chapter 3 of the April 2018 World Economic Outlook by Wenjie Chen, Bertrand Gruss, Nan Li, Weicheng Lian, Natalija Novta, and Yu Shi.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Emerging TechnologiesSee all

Gareth Francis

July 14, 2025

David Elliott

July 14, 2025

Babak Hodjat

July 11, 2025

Markus Kirchschlager and Benedikt Gieger

July 10, 2025

Victoria Masterson, Ian Shine and Madeleine North

July 10, 2025

Gayle Markovitz and Beatrice Di Caro

July 9, 2025