Are we in a corporate debt bubble?

Since 2007, the value of corporate bonds outstanding from nonfinancial companies has nearly tripled.

Image: REUTERS/Toby Melville

Susan Lund

Vice-President, Economics and Private Sector Development, International Finance CorporationStay up to date:

Financial and Monetary Systems

In the decade since the global financial crisis, the value of nonfinancial companies' outstanding bonds has nearly tripled, owing not least to growth in corporate debt in emerging markets. But while a correction seems likely as defaults rise, the broad shift toward bond financing is actually a welcome development.

Is growing corporate debt a bubble waiting to burst? In the ten years since the global financial crisis, the debt held by nonfinancial corporations has grown by $29 trillion – almost as must as government debt – according to new research by the McKinsey Global Institute. A market correction is likely in store. Yet the growth of corporate debt is not as ominous as it first appears – and, indeed, in some ways even points to a positive economic outcome.

Over the past decade, the corporate-bond market has surged as banks have restructured and repaired their balance sheets. Since 2007, the value of corporate bonds outstanding from nonfinancial companies has nearly tripled – to $11.7 trillion – and their share of global GDP has doubled. Traditionally, the corporate-bond market was centered in the United States, but now companies from around the world have joined in.

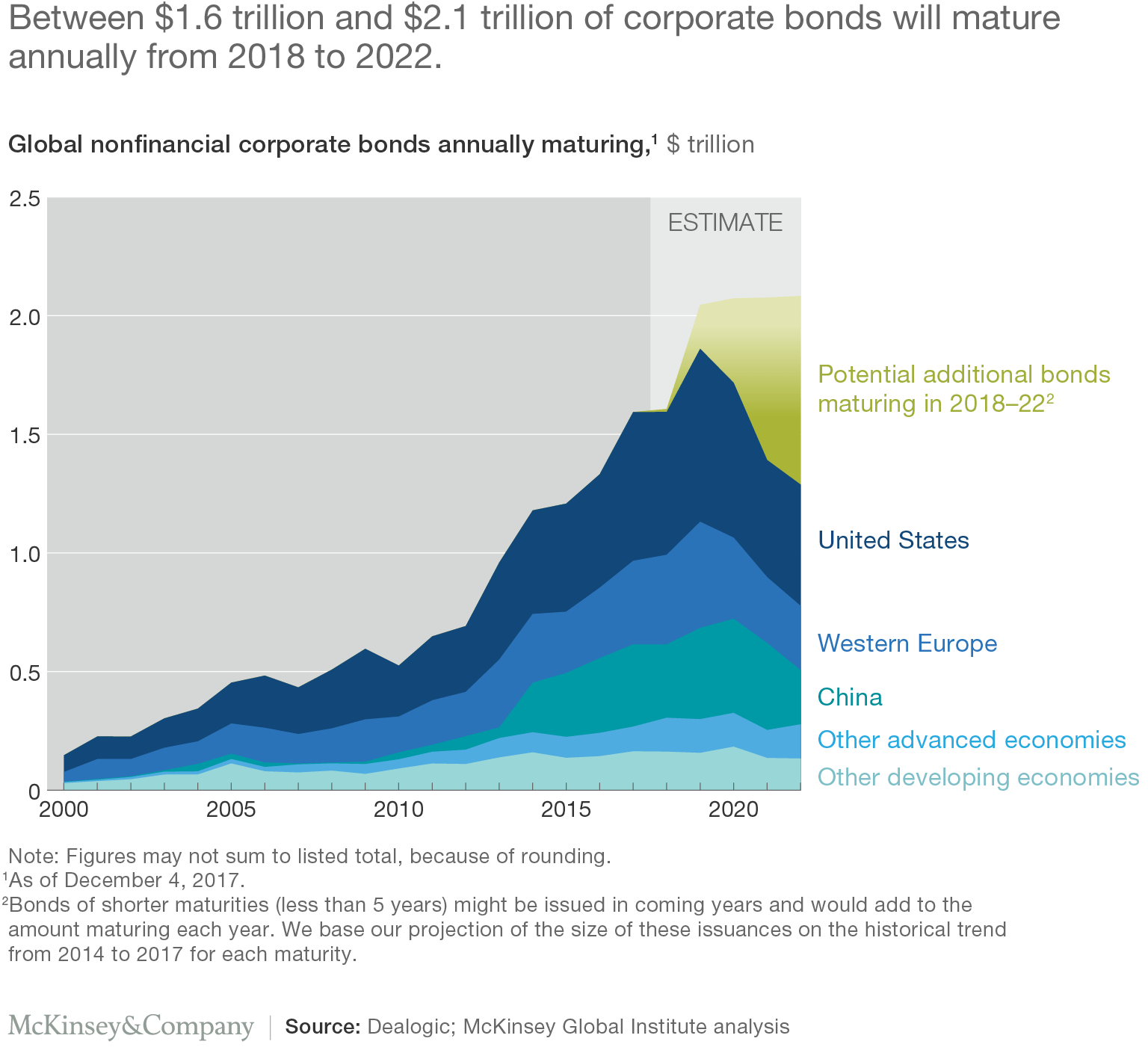

The broad shift to bond financing is a welcome development. Debt capital markets provide an important asset class for institutional investors, and give large corporations an alternative to bank loans. Yet it is also clear that many higher-risk borrowers have tapped the bond market in the years of ultra-cheap credit. Over the next five years, a record $1.5 trillion worth of nonfinancial corporate bonds will mature each year; as some companies struggle to repay, defaults will most likely rise.

The average quality of borrowers has declined. In the US, 22% of nonfinancial corporate debt outstanding comprises “junk” bonds from speculative-grade issuers, and another 40% are rated BBB, just one notch above junk. In other words, nearly two-thirds of bonds are from companies at a higher risk of default, including many US retailers. These businesses have a lot of speculative-grade debt coming due over the next five years, and for many the math simply will not add up, owing to declining sales as shoppers go online.

Another potential source of vulnerability is soaring corporate debt in developing countries, which have accounted for two-thirds of overall corporate-debt growth since 2007. In the past, advanced-economy firms were the largest borrowers. But much has changed with the rise of China, which is now one of the largest corporate-bond markets in the world. Between 2007 and the end of 2017, the value of Chinese nonfinancial corporate bonds outstanding increased from just $69 billion to $2 trillion.

One final source of risk is the fragile finances of some bond-issuing companies. To be sure, MGI finds that in advanced economies, less than 10% of bonds would be at higher risk of default if interest rates were to rise by 200 basis points. Similarly, in Europe, the share of bonds issued by at-risk companies is currently less than 5% in most countries, indicating that only the largest blue-chip companies have issued bonds so far.

The problem is that there are pockets of vulnerability. Even at historically low interest rates (before the US Federal Reserve raised its benchmark rate to 1.75-2% on June 14), 18% of bonds (worth roughly $104 billion) outstanding in the US energy sector were at higher risk of default.

Still, the biggest risks appear to be in emerging markets such as China, India, and Brazil. Already, 25-30% of bonds in these markets have been issued by companies at a higher risk of default (defined as having an interest-coverage ratio of less than 1.5). And that share could increase to 40% if interest rates were to rise by 200 basis points.

Within these emerging markets, some sectors are more vulnerable than others. In China, one-third of bonds issued by industrial companies, and 28% of those issued by real-estate companies, are at a higher risk of default. Corporate defaults are already creeping upward in China; and in Brazil, one-quarter of all corporate bonds at a higher risk of default are in the industrial sector.

With the global corporate default rate already above its 30-year average and likely to rise further as more bonds come due, is the next global financial crisis at hand? The short answer is no. While individual investors in bonds may face losses, defaults in the corporate-bond market are unlikely to have significant ripple effects across the system, as the securitized subprime mortgages that sparked the last financial crisis did.

Beyond the near-term bumps in the road, the shift to bond financing by companies is a positive development. There is plenty of room for further sustainable growth. But as the market grows, banks will need to rethink their strategies focusing more on other customer segments, such as small and medium-size businesses and households. Investors and individual savers, for their part, will have new opportunities for portfolio diversification.

But if the financial crisis ten years ago taught us anything, it is that risks often emerge where they are least expected. That is why regulators and policymakers should continue to monitor existing and potential risks, such as those arising from credit default swaps on corporate borrowers or complex securitization of bonds. They should also welcome the establishment of electronic platforms for selling and trading corporate bonds, to create more transparency and efficiency in the marketplace. That way, today’s debt would be less likely to become tomorrow’s debt overhang.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Respectful national partnerships key to achieving impact and efficiency in international development

Ruth Goodwin-Groen, Pia Bernadette Roman Tayag, Hinjat Shamil and Tidhar Wald

May 5, 2025

Ana Mahony

April 30, 2025

Graham Pearce

April 30, 2025

Rebecca Geldard

April 29, 2025

Michael Eisenberg and Francesco Starace

April 25, 2025