Why is wage growth still slow?

Image: REUTERS/Ints Kalnins

Stay up to date:

United States

The failure of wages to recover to their pre-recession growth rates in the developed world has been a continuing puzzle for economists. Although output has grown significantly in most of these countries, real wages have recovered much more slowly (e.g. Jowett et al. 2014). Nominal wage growth has been weak so that real wages have hardly risen even though price inflation has also been sluggish. In this column, we summarise the importance of underemployment in explaining this low wage growth based on work in a recent paper (Bell and Blanchflower 2019).1

The traditional explanation would be that wage growth was held back by high levels of unemployment. But this explanation is not consistent with the facts. Unemployment rates are low especially in the US (3.9% in August 2018) and the UK (4.2% in May 2018) and Germany (3.4% in July 2018). However, they remain in double digits in Italy (10.4%), Spain (15.1%) and Greece (19.5%) and average 8.2% in the euro area. The search for alternative explanations of weak wage growth has focused attention on underemployment, as measured by the willingness of current workers to increase their working time without increasing their wage rate. In contrast to unemployment, the underemployment rate has not returned to pre-recession levels in the US and the UK in particular.

In our interpretation of the concept, underemployment implies workers are off their labour supply curves, in contrast to the so-called canonical model which suggests workers are free to choose their hours of work, given the wage rate, and so are on their labour supply curves. This model assumes that workers select from a continuum of hours, while treating the wage rate as exogenous, continues to dominate research and teaching. This approach persists, even though aggregate hours fluctuate in response to changes in demand and the organization of production requires employers to place some restrictions on working time, for example, to ensure that a production line is fully staffed.

Involuntary part-timers

The most widely available measure of underemployment estimated by statistical agencies around the world – such as the Bureau of Labor Statistics in the US, the Office for National Statistics in the UK, and the EU statistical agency Eurostat – is the share of involuntary part-time workers in total employment. This measure only captures the number of part-time workers that wish to extend their hours. It carries no information on the number of additional hours these workers wish to work, nor if some (other) workers, including voluntary part-timers and full-timers, would prefer to reduce their hours.

However, the widespread use of this measure of underemployment reflects the lack of alternatives, particularly in the US. In Europe, involuntary part-timers are described as part-timers who want full-time jobs (PTWFT), whereas in the US they are described as part-time for economic reasons (PTFER). In Europe, statistics on PTWFT are obtained from the individual level European Labor Force Surveys (EULFS) and in the US on PTFER from the Current Population Survey. We treat these measures analogously.

Figure 1 plots the involuntary part-time measure as a percent of total employment that we call U7 for both the US and the UK. The most recent UK rate of 3.0% for May 2018 remains above pre-recession lows of 2.3% found in May 2008 and the historic low of 1.9% found in six separate months in 2004 and one in 2005. The US rate in August 2018 was 2.8% below the December 2007 rate of 3.2% but above the series low of 2.3% found in seven separate months in 2000. The question remains how low the involuntary part-time rate can go without generating rapidly rising wage pressure.

Figure 1 Involuntary part-time as % of employment (U7) in the UK and US, January 2006-May 2018

The Bell/Blanchflower underemployment index

Measuring underemployment using the involuntary part-time rate does not fully capture the extent of worker dissatisfaction with currently contracted hours. It turns out that over the Great Recession years and subsequently, not only do part-timers who say they would prefer full-time jobs want additional hours, but voluntary part-timers and full-timers do too. Indeed, some voluntary part-timers and full-timers say they want fewer hours. The numbers of additional hours of those who wanted more rose over time and the number of hours who wanted less, fell in the downturn, only to reverse those trends during recovery.

In the EULFS, workers report whether they would like to change their hours at the going wage rate and how many extra or fewer hours they would like to work. A desired hours variable can thus be constructed for each individual. It is set to zero for workers who are content with their current hours. It is negative for those who wish to reduce their hours (the overemployed) and positive for the underemployed who want more hours. The data are nationally representative and hence we sum them into millions of hours and deduct the number of hours of those who want less hours from the number that want more to generate a measure of excess hours. We translate it into unemployment equivalents by dividing by average hours worked by the employed.

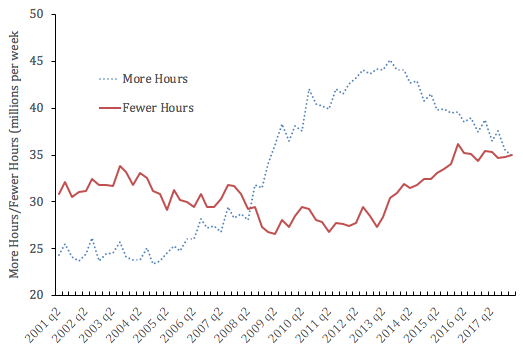

Figure 2 shows our estimates for the UK of the number of desired hours of those who want more hours (the underemployed) and those who want less (the overemployed) at the going wage. The latter series was broadly flat until recently but was always above the fewer hours series before 2008. That suggests there is still a good deal of under-utilized resources in the labour market available to be used up before the UK reaches full-employment. There has been a rise both in the number of hours of those who want more hours and those who want less in the post-recession years.

Figure 2 More and fewer desired hours in the UK, 2001Q2 - 2018Q1

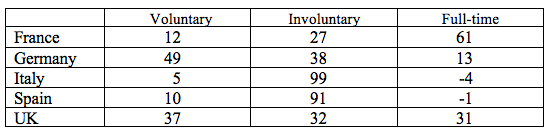

Table 1decomposes the net variation in aggregate desired hours – which deducts the number of hours the overemployed desire from the number the underemployed desire – into components from voluntary and involuntary part-timers, and full-timers using the EULFS for 2016. Our paper reports estimates, for other years and additional European countries. It is clear that the extent to which IPTR is a biased estimator of the extent of labour market slack in the period after the Great Recession varies by country. In France 27% of the excess is due to involuntary part-timers versus 99% in Italy.

Table 1 Share of excess hours, 2016 (%)

The extent of the bias will move over the business cycle and remains uncertain in the US that does not have such data. We also note the relatively low incidence of part-time work in the US may mean the proportion of workers who are PTFER will likely further underestimate of underemployment in the US.2

Wages, unemployment, and underemployment

We explore the issue of underemployment reducing wage pressure further for the UK, an international panel of 31 countries as well as for the US where we only have data on PTFER available. In the case of the UK we found that wage growth was significantly lowered, in a quarterly regional panel by an underemployment measure, the log of the number of additional hours the underemployed would like. The unemployment rate was insignificant. In an unbalanced international panel of 28 countries from 1976-2016 we found that involuntary part-time employment lowered wage growth confirming IMF results using these data from Hong et al. (2018).

We then examined wage growth in the US using wage data from the Merged Outgoing Rotation Group files of the Current Population Survey from 1979-2017. Consistent with the findings of Blanchflower and Oswald (1994), we found that for the period 1980-2017 the unemployment rate enters negatively in a wage growth equation. However, in the years since the Great recession the unemployment rate was insignificant, but an underemployment measure (U7) – PTFER as a percent of employment – was significantly negative. This was true whether weekly or hourly earnings were used. In contrast to the unemployment rate (U3), the U7 variable still remains elevated and predicts weak wage growth.

We also find evidence that the change in the home ownership rate enters significant and positive in wage growth equations. In the years that we have data for from 1985 through 2005, 16 years had positive changes. From 2005-2016 all were negative and 2017 was positive again. A rising home ownership raised wage growth in the pre-recession years; falling home ownership rates lowered wage pressure in the pre-recession years.

So what?

It seems the US and the UK are a long way from full employment. Policymakers should not be focused on the unemployment rate in the years post-recession, but rather on the underemployment rate. The underemployment rate remains elevated in many countries in contrast to the unemployment rate. Declining home ownership has also helped to contain wage growth. Underemployment replaces unemployment as the main measure of labour market slack in the post-recession years.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Jobs and the Future of WorkSee all

Steffica Warwick

July 3, 2025

Ibrahim Odeh and Oliver Tsai

July 2, 2025

Ravi Kumar S. and Rohan Murty

July 1, 2025

Abayomi Olusunle

July 1, 2025

Ian Shine

June 27, 2025