The impact of population ageing on monetary policy

An ageing population can have a range of negative effects on a country's economic performance.

Image: REUTERS

Stay up to date:

Financial and Monetary Systems

Many countries, developed and developing alike, are experiencing a process of population ageing – fertility rates remain below the level that guarantees the replacement of the population and the average life expectancy at birth keeps increasing. As a consequence, the ratio of the elderly to the working-age population – the old age dependency ratio – has been, and will be, increasing over the upcoming decades. To give some idea on the magnitude of this process, while the ratio of elderly (aged 65 or more) to the working-age population (aged 15-64) in the euro area was around 0.25 at the turn of the 21st century, the proportion is projected to exceed 0.5 by 2050 (see Figure 1).

The demographic transition will have many consequences related to various aspects of economic activity. To mention just a few, the increasing share of elderly in populations is likely to negatively impact the growth rate of GDP per person (Cooley and Henriksen 2018) and the sustainability of pension systems (Boulhol and Geppert 2018), and will lead to an increase in the share of GDP being spent on healthcare and related services (Breyer et al. 2011).

What is perhaps less clear is whether these processes should be of first-order significance to central banks. It is tempting to conclude that the glacial speed of demographic changes makes them irrelevant for monetary policy (e.g. Bean 2004, Kara and von Thadden 2016). In a recent paper (Bielecki et al. 2018) we quantify the impact of demographic trends on the euro area economy and argue that their implications for the conduct of monetary policy should not be neglected. Our argument is based on a life-cycle model of the euro area households, which we feed with past and projected data on demographic processes about fertility rates and mortality risk in the euro area, based on the Eurostat estimates for the past and EUROPOP projections for the next decades.

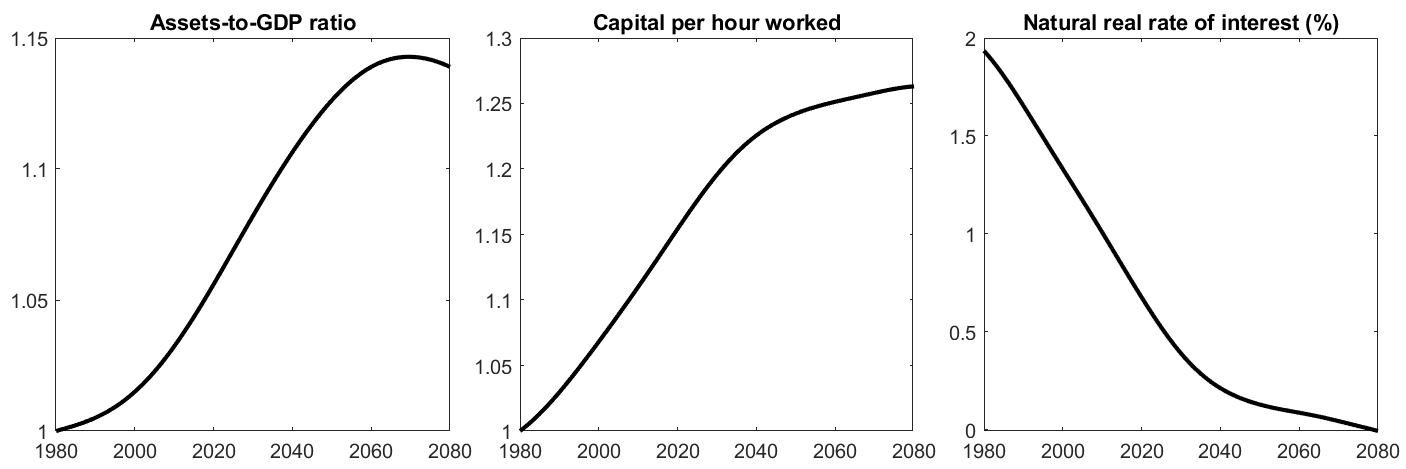

The obtained macroeconomic effects of population ageing are depicted in Figure 2. In response to an increase in the expected life duration, households choose to increase the rate at which they accumulate assets prior to retirement. Additionally, due to a falling share of working-age adults in the total population, capital becomes relatively abundant. According to our estimates, these two forces lead to an increase in the assets-to-GDP ratio by 8% between 1980 and 2030, and to a rise in the level of capital per hour worked by 20% over the same period. This drives the natural real rate of interest (NRI) from almost 2% in 1980 down to 0.4% in 2030. The estimated magnitude of this fall in the euro area NRI is slightly larger to that obtained for a group of developed countries (Carvalho et al. 2016).

The NRI is a key object from the point of view of monetary policy. If the central bank is able to adjust its policy rate such that the real interest rate perfectly tracks the NRI, then (absent cost-push shocks to the economy) output is at its potential level and inflation is at the central bank’s target. For a given inflation target, the level of the NRI determines the average distance of the nominal interest rate from the zero lower bound (ZLB). Hence, the demographic transition poses a challenge for monetary policy as, by lowering interest rates, it raises the probability of the constraint materialising. This possibility has been widely discussed in the theoretical literature (Eggertsson et al. 2019), and we offer a quantitative assessment of the contribution of demographic trends. According to our estimates, while the probability of hitting the ZLB constraint was below 0.5% in annual terms in 1980, due to demographic developments it increased to almost 3% by 2015 and is projected to rise to around 4% by 2030 (solid line in the left-hand panel in Figure 3). This process looks even more dramatic if one compares probabilities for longer periods. We estimate the chance of hitting the ZLB at least once during the 1980s to be approximately 4%. Due to demographic changes, this is expected to increase to over 30% in the 2020s.

Importantly, these estimates assume that the central bank observes the evolution of the NRI in real time. The NRI is a latent variable, however, and is usually inferred from past data with some lag. Our additional simulations take this fact into account. When we assume that the central bank learns gradually about changes in the NRI, our model implies that such imperfect knowledge creates a sizable deflationary bias. If the NRI exhibits a secular downward trend but the central bank learns about it only from past data, it will overestimate its level. As a result, the monetary policy stance will tend to be too contractionary. Consequently, our model suggests inflation remaining up to 0.35 percentage points below the target (dashed line in the right-hand panel of Figure 3). Since lower inflation results in lower nominal interest rates, the deflationary bias resulting from ignoring demographic trends implies an even greater probability of monetary policy being constrained by the ZLB (Figure 3, left panel). In this case the probability of hitting the ZLB rises to 6.5% in 2030, and the chance of monetary policy being constrained for at least one year in the 2020s is around 45%.

Two key assumptions underlie our results: we assume that the retirement age is held constant, and that the central bank’s inflation target does not change. An increase in the minimum eligibility retirement age would reduce the expected number of years lived while relying on non-labour capital income to support consumption. This would alleviate the need to accumulate more assets prior to retirement, and at the same time increase the number of hours worked per person in the economy. Both of those changes would reduce the downward pressures on the NRI. Alternatively, one could possibly consider increasing the central banks’ inflation target, although this would involve additional costs associated with higher average inflation rates. Nevertheless, if we want to avoid the painful periods during which monetary policy is constrained in its ability to adjust the nominal interest rates, some sort of policy adjustment might be unavoidable.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Spencer Feingold

April 17, 2025

Lucia Fry and Naomi Nyamweya

April 17, 2025

Spencer Feingold

April 15, 2025

Hubert Keller and Maximilian Martin

April 15, 2025

Makaio Witte and Sourajit Aiyer

April 14, 2025

Tariq Bin Hendi

April 8, 2025