This new form of currency could transform the way we see money

Emerging economies may have the most to gain by introducing Central Bank Digital Currency.

Image: REUTERS/Derick Snyder

Stay up to date:

Financial and Monetary Systems

Central banks around the world are experimenting with so-called Central Bank Digital Currency (CBDC). But what is it and why does it matter?

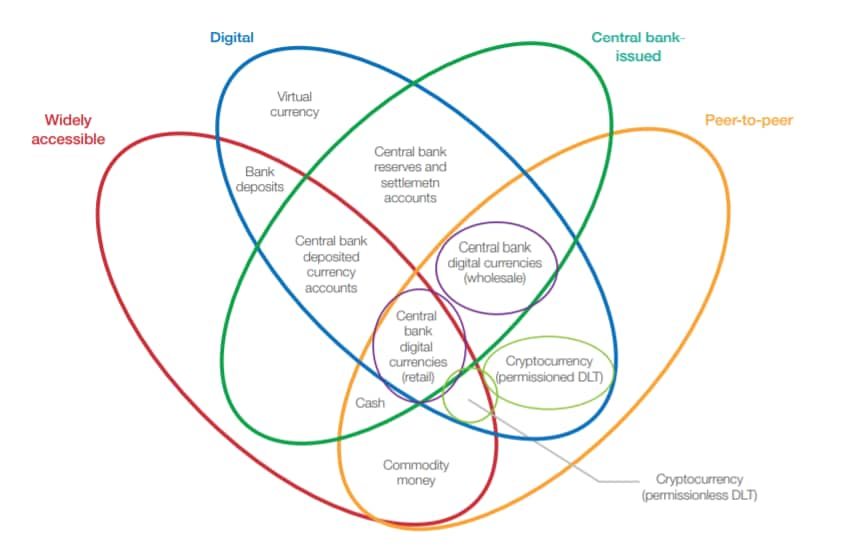

CBDC is a digitized version of domestic currency where the central bank issues new money equivalent to – and redeemable for – its domestic currency, often removing the equivalent amount of currency from the money supply.

It could be issued using distributed ledger technology, where transactions would operate and settle on a peer-to-peer basis. CBDC can also be issued using traditional centralized technologies.

CBDC may be issued for general use (“retail” CBDC) for peer-to-peer payments and payments from consumers to merchants; or for use by commercial banks and clearing houses (“wholesale” CBDC) for more efficient interbank payments that occur outside traditional correspondent banking and other payment systems.

While it may seem far-fetched, at least 44 central banks, according to survey research by the BIS, are currently or will soon be researching and experimenting with CBDC.

Research underway

The fact that dozens of central banks are exploring, and in some cases implementing, CBDC based on blockchain technology is significant, and is an early indicator of the potential use of this emerging technology across financial and monetary systems.

Central banks play one of the most critical roles in the global economy, and their decisions about implementing distributed ledger and digital currency technologies in the future can have far-reaching implications for economies.

Regardless of the breadth of research underway, conclusions are yet to be drawn by most central banks and need to be made on a country-by-country basis. In some cases, CBDC has the potential to improve current systems. In other cases, many central banks may find that it is not worth the investment. The central bank of Denmark, for instance, says in a 2017 report: “In a Danish context, it is unclear what central bank digital currency would be able to contribute that is not already covered by the current payment solutions.”

Emerging economies might benefit most

Emerging country central banks may experience the greatest gains from the implementation of distributed ledger technologies where existing financial processes and technology systems are not yet highly efficient or deeply rooted. They may also achieve greater financial inclusion from implementing CBDC.

The Bank of Thailand and the South African Reserve Bank, among others, are experimenting with CBDC in large-scale pilots for interbank payment and settlement efficiency. The Eastern Caribbean Central Bank is exploring the suitability of distributed ledger technologies to advance multiple goals, from financial inclusion and payments efficiency to payment system resilience against storms and hurricanes.

The National Bank of Cambodia will be one of the first countries to deploy blockchain technology in its national payments system for use by consumers and commercial banks. It is implementing blockchain technology in the second half of 2019, as an experiment to support both financial inclusion and greater banking system efficiency.

Over the next four years, we should expect to see many central banks decide whether they will use blockchain and distributed ledger technologies to improve their processes and economic welfare. Given the systemic importance of central bank processes, and the relative immaturity of blockchain technology, central banks need to carefully consider all known and unknown risks to implementation.

The two types of CBDC

Wholesale CBDC – The leading cases for wholesale CBDC, which is made available only to commercial banks and clearing houses for use in the wholesale interbank market, consist of increasing efficiency in domestic or cross-border interbank payments. Today, these processes in some countries can be inefficient and entail costs, time, and counterparty risks to banks.

Most early-stage CBDC central bank pilots thus far have focused on wholesale CBDC for domestic use. By employing this type of digital currency, central banks hope to achieve increased efficiency in interbank payments and in interbank securities trading and settlement. Central banks from several countries are experimenting with this version of CBDC, including those from South Africa, Canada, Japan, Thailand, Saudi Arabia, Singapore, and Cambodia.

Retail CBDC – The leading cases for retail CBDC, which is made widely available to the public, relate to the ability to potentially increase financial inclusion, or to serve as a strategic alternative to physical cash in economies where cash dwindles.

CBDC acts as a substitute or complement for cash and an alternative to traditional bank deposits. For some countries, this form of digital currency could have the potential to incentivize participation in the banking sector for the under-banked, improve peer-to-peer and overseas payments, and potentially improve KYC/AML functionalities or curb illicit activities. In regions with decreasing use of cash, it could serve as an important counterweight to retail payment applications developed by the private sector.

Central banks from several countries are experimenting with this form of CBDC, including those from the Eastern Caribbean, the Bahamas and Cambodia. Importantly, CBDC can also be issued in a centralized manner without blockchain technology. Sweden has been evaluating both forms of CBDC.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Tariq Bin Hendi

April 8, 2025

Jeremy Jurgens

April 7, 2025

Rebecca Geldard

April 1, 2025

Aaron Schumm

March 31, 2025

Jon Jacobson

March 27, 2025

Adolfo Garcia and Fernando Johann

March 27, 2025