Bangladesh faces a crisis in remittances amid COVID-19

Remittances from Bangladeshi migrant workers are expected to fall by 25% this year.

Image: REUTERS/Edgar Su

Stay up to date:

Migration

- The coronavirus pandemic highlights the need for better cooperation over migration.

- Bangladesh has offered incentives to encourage expatriate workers to send their money through legal channels.

- Public bodies and remittance services providers must improve access to digital solutions.

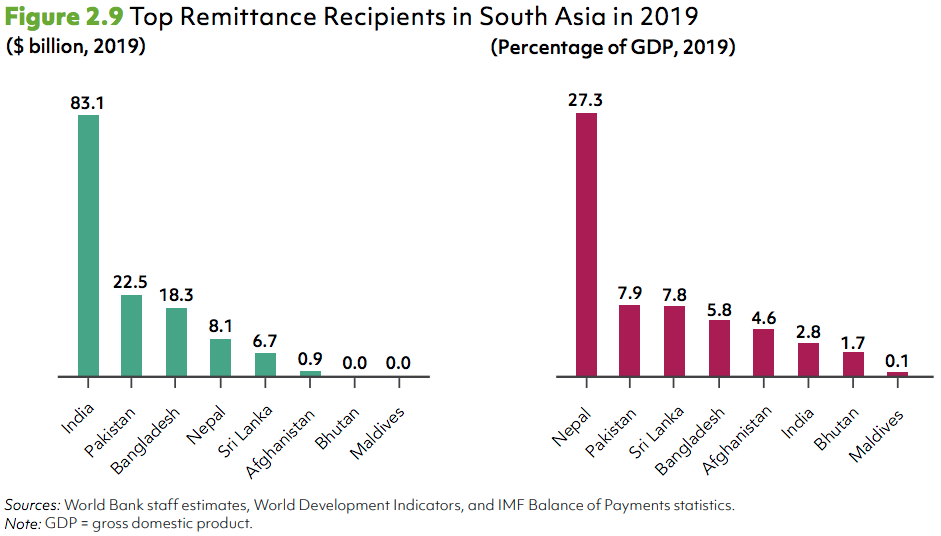

The economic importance of the more than 10 million migrants from Bangladesh who sent close to $18 billion in 2019 cannot be overstated. International remittances normally represent around 7% of Bangladesh’s GDP. But the COVID-19 pandemic is having an acute effect on Bangladeshi migrants abroad, who are largely concentrated in countries with strict lockdown measures. Considering the large volume of Bangladeshi migrants in the Middle East, secondary economic impacts through depressed demand and falling oil prices will also likely add strain to the flow of remittances.

World Bank estimates have projected that total remittances by migrant workers from Bangladesh will fall to $14 billion for 2020 – around a 25% decrease from the previous year. Figures released by Bangladesh Bank show that year-on-year remittances for the month fell by 25%, indicating that the World Bank’s projection is, unfortunately, likely to hold true. The drop in these payments, which have traditionally averaged between $300 and $600 a month, will represent a significant loss to millions of household incomes in Bangladesh.

Crisis exposes need for better migration cooperation

The need to halt the falling flow of remittances in the country must start with a conversation about migration.

Mostly working in the tourism, hospitality and construction sectors, many migrants to the Gulf have been laid off and face limited prospects for employment. With coronavirus outbreaks emerging in the Gulf states, and more recently in Singapore, it has been reported that the pandemic has been experienced mostly among these migrant workers – living in crowded, dormitory-style labour camps, they are especially vulnerable to COVID-19.

The response to the crisis among a number of countries, including Bahrain, Kuwait, the Maldives, Qatar, Saudi Arabia and the United Arab Emirates, has been to compel or to put pressure on countries like Bangladesh to repatriate their migrant workers. Bangladesh has been hesitant to bend to these demands amid the public health risks. And when travel restrictions are lifted, the return of newly unemployed migrants could overwhelm the country’s economy.

It has therefore become imperative that Bangladesh mobilizes its diplomatic corps to ensure that there is greater migration cooperation, not only during the current lockdown phase but also during the COVID-19 recovery phase. Shahidul Haque, Bangladesh’s former foreign secretary, urged that strategies to defeat the coronavirus must emphasize “inclusiveness, courage and collaboration, without distinction or discrimination” – or they will “not succeed”. Mr Haque added: “A holistic, nuanced approach that acknowledges migrants’ economic contributions is optimal.”

Policy actions taken to ensure money flows

On the stimulation of domestic entrepreneurship in Bangladesh, the government has already taken proactive measures. It is encouraging that the government has already allocated Tk 30.6 billion ($361 million) as incentives in the budget for this fiscal year to encourage expatriate workers to send their money through legal channels. Some of the banks are also providing an extra 1% incentive for remittance beneficiaries, further increasing the attractiveness for remitters.

To finance some of its efforts, Bangladesh has been looking to mobilize its development partners. Initial financing of $150 million from the Asian Development Bank has been supplemented by a loan for another $500 million. Bangladesh Bank is making efforts to ensure liquidity in the market while keeping the foreign exchange rate stable. The central bank should be commended for also increasing the ceiling for expatriate Bangladeshis on remittances that give a 2% cashback (more than tripling the ceiling to $5,000; Tk 500,000).

Judging by the success of the incentive scheme introduced by the government last year, the Ministry of Finance should look to extend this out for the next fiscal year during the upcoming budget cycle. For remittances originating in key markets such as Malaysia, Saudi Arabia, the United Arab Emirates and the United Kingdom, it should also look to increase this cash incentive from 2% to 4%.

Digitization and the role of remittance service providers

Despite the presence of many modern service providers, the most popular way to send remittances has remained taking cash in person to a sending agent – yet the pandemic has severely disrupted this.

A survey of senior executives in the remittances industry has shown acute COVID-19 impacts in South Asia. It also reveals insights for digital solutions that require no interactions with an agent. Conducted in March 2020 by the International Association of Money Transfer Networks (IAMTN) in collaboration with the United Nations Capital Development Fund (UNCDF), the survey revealed that Saudi Arabia, the United Arab Emirates, United Kingdom and United States were the countries most impacted by outbound remittances. Together, these usually account for half the remittance inflows to Bangladesh. The adoption of digital solutions at both the sending and receiving ends may ensure at least access for migrants and families who so clearly need these remittances (even while the economic conditions for Bangladeshi migrant workers in such countries will be likely to keep the amounts depressed).

The opportunity of transitioning migrants and their families to the use of digital solutions such as mobile phone apps cannot be realized by providers alone. A coordinated effort can be made between public-sector institutions and remittance services providers to reach out to migrants and their families in order to help them open bank accounts, and to improve access to digital solutions. Banks and mobile money providers should be encouraged to implement Bangladesh’s guidance on electronic “know your customer” requirements (e-KYC). Efforts are needed to ensure interoperability between mobile financial services, since this can play an important role in improving inward remittances through mobile accounts. Appropriate measures may also be needed to ensure that any transaction fees for transferring remittances from mobile wallets to bank accounts are waived.

The government can create incentives to the banks, remittance service providers, mobile operators and other enablers of the remittance flows to ensure providers can financially sustain their operations, maintain the agent networks, and also extend benefits to the customers. Remittance service providers themselves can make accounts more attractive to Bangladeshis by providing value-added services, such as linking remittances with savings, credit, insurance, payments, and other inclusive financial products tailored to the needs of migrants and their families. The termination of remittances in digital wallets, and incentives against cash-outs, can also help greatly. For example, a partnership between mobile financial services providers with local commercial banks is allowing inward flows via online-to-wallet money-transfer companies, reportedly increasing the daily average sent by expatriates by as much as 150% in April 2020.

The fact that the current crisis has had such a negative impact on migrant workers’ incomes highlights the need for digital progress to improve resilience and maintain vital flows of money for low-income populations.

What is the World Economic Forum doing to manage emerging risks from COVID-19?

A call to action

As with other sectors, public-private cooperation will remain key in mitigating the impact of COVID-19 on the remittances industry. A high-level call to action has already been spearheaded by the governments of Switzerland and the United Kingdom, as jointly announced on 22 May 2020 by UNCDF and the United Nations Development Programme (UNDP). The “Remittances in Crisis – How to Keep Them Flowing” call to action is supported by KNOMAD, the World Bank, the International Organization for Migration (IOM) and the International Association of Money Transfer Networks (IAMTN), and International Chamber of Commerce (ICC). Since it was announced, key member states receiving a high-volume of remittances across regions – Mexico, Ecuador, El Salvador, Jamaica, Egypt, Nigeria, Zimbabwe, and Pakistan – have also joined the call to action.

The joint statement reads: “By building capacity for a conducive regulatory and policy environment, strengthening open digital payment ecosystems, and fostering innovation for inclusive digital solutions for migrants, UNCDF and UNDP are supporting governments and the private sector to ensure continuity in the remittance flows to the countries and families hardest hit by the effects of the coronavirus.” There is a lot that can be achieved in support of the Bangladeshi migrants and their families who, home and abroad, contribute so very much.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Health and Healthcare SystemsSee all

Shyam Bishen

May 27, 2025

Daniella Diaz Cely

May 27, 2025

Silvio Dulinsky

May 23, 2025